$920 billion needed to bridge the ‘great raw material disconnect’: Benchmark CEO Simon Moores

:format(auto):focal(center))

The following is a speech given by Benchmark’s chief executive Simon Moores at the opening of the Battery Gigafactories USA 2023 conference in Washington, DC.

Today, we must recognise that for our industry this is a moment.

This global battery arms race has arrived on these shores at a pace we could have never imagined, even only 18 months ago.

It is especially a moment for the critical mineral explorers, developers, miners, and refiners. That’s the hardest job in the industry – it’s a thankless task for the prospectors, developers and pioneers that actually go around the world and look for these minerals and put in the real hard work to actually attempt to bring them to production.

It’s the hardest job in the supply chain but it’s absolutely all eyes on that sector now, and it’s deserved.

Having been focused on this my whole career – since 2006 and with Benchmark since 2014 – I have never seen this level of interest and such a window of opportunity that we have now for building critical mineral mines and refining plants in the US.

And we all know this is thanks to the inflation reduction act, which has now been handed a 17-month window, a 17-month bull market to actually make it happen, thanks to the debt ceiling agreement being made.

In the last 12 months has turbo charged this lithium ion economy in the US.

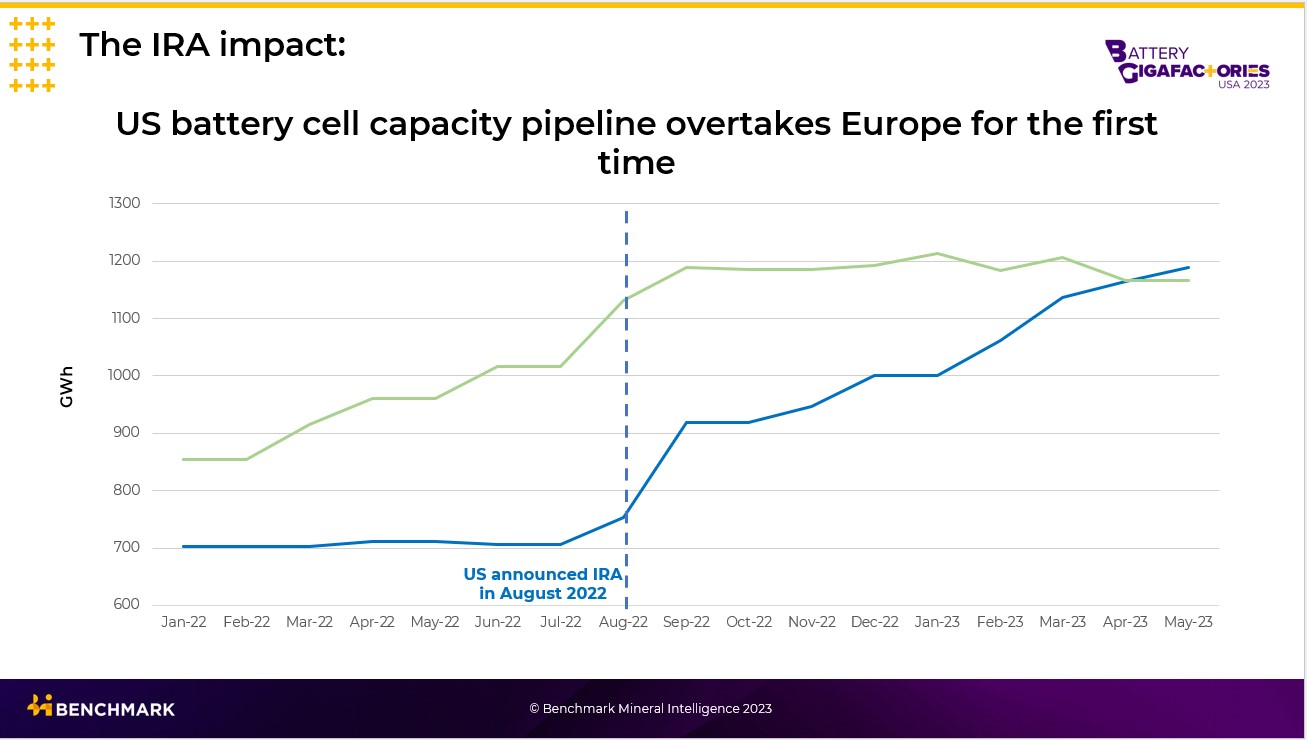

IRA helps US overtake Europe

This first chart here is the impact of the Inflation Reduction Act, announced last August … No wonder the European Union are terrified of investment money flowing towards North America and free trade countries.

It’s interesting geopolitical development that those two regions are trying to bridge the gap.

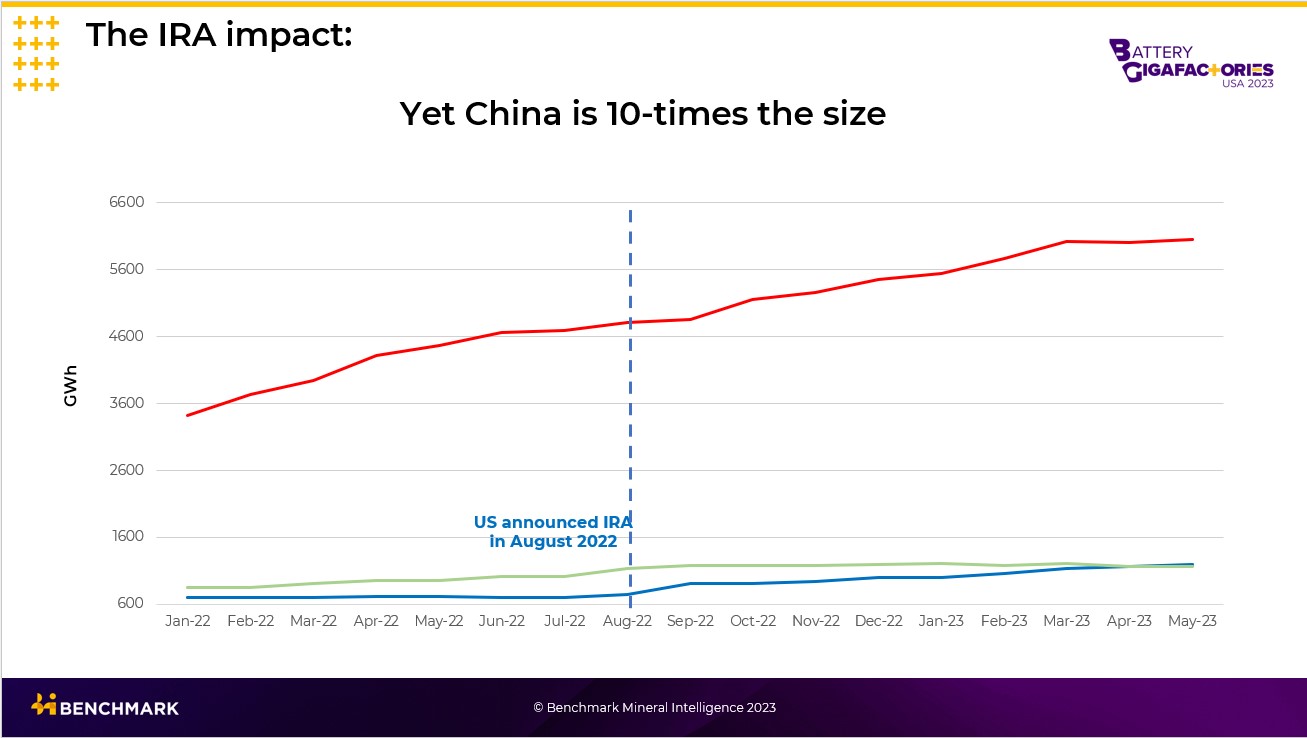

But let’s not forget China is 10 times the size of what’s happening and what’s happening in Europe. It’s a different ballgame what’s happening in China. They are the true pioneers of this industry, building the supply chains, building at scale and speed … it’s a huge gulf.

It is incredible to see how important geopolitically this industry has become. We kind of scratch ourselves and try and work out how this has gone right to the top of the geopolitical agenda.

The geopolitical, industrial and technological tailwinds all now move in the same direction from east to west.

Lithium ion batteries and electric vehicles are an industrial pillar of the 21st century and they are the centre point of this energy transition.

You can talk about other technologies but in terms of building from scratch lithium ion batteries, sit right in the middle, right in the crux of this whole movement.

The critical mineral supply chains that fuel these industries are as geopolitically important as the oil pipelines of today and in the agendas of governments they are above that industry – that’s how important it’s got.

Lithium, nickel, graphite, cobalt, manganese, copper, rare earths, phosphate, and fluorspar – mastering these supply chains to various degrees will make or break a nation’s industrial direction for this century.

We’re nearly 25 years into this century – this is a movement that’s going to last a long long time.

A gigafactory without critical minerals and chemicals is about as useful as grain silo to EV makers. Without a secure raw material pipelines into these gigafactories they’re useless.

Battery makers, OEMs, and indeed countries – especially the world’s leading economy here in the US – need joined-up thinking for this.

If you are a battery or EV maker you need to think like a miner and chemical producer. We’re starting to see this mix of cultures happen now but it’s been a long time coming.

China’s dominance

China has led the way for the best part of the last 10 years on this.

China’s forward thinking and aggressive industrial strategy to build gigafactories, chemical and critical mineral refining plants has ensured the flow of the world’s key raw materials is towards China.

As a result, huge downstream value is created.

Today, benchmark data shows 80% of the world’s lithium ion batteries are made in China.

Over 80% of cathode is made in China.

90% of anode is made in China.

The most critical part for me is the strategy on critical minerals.

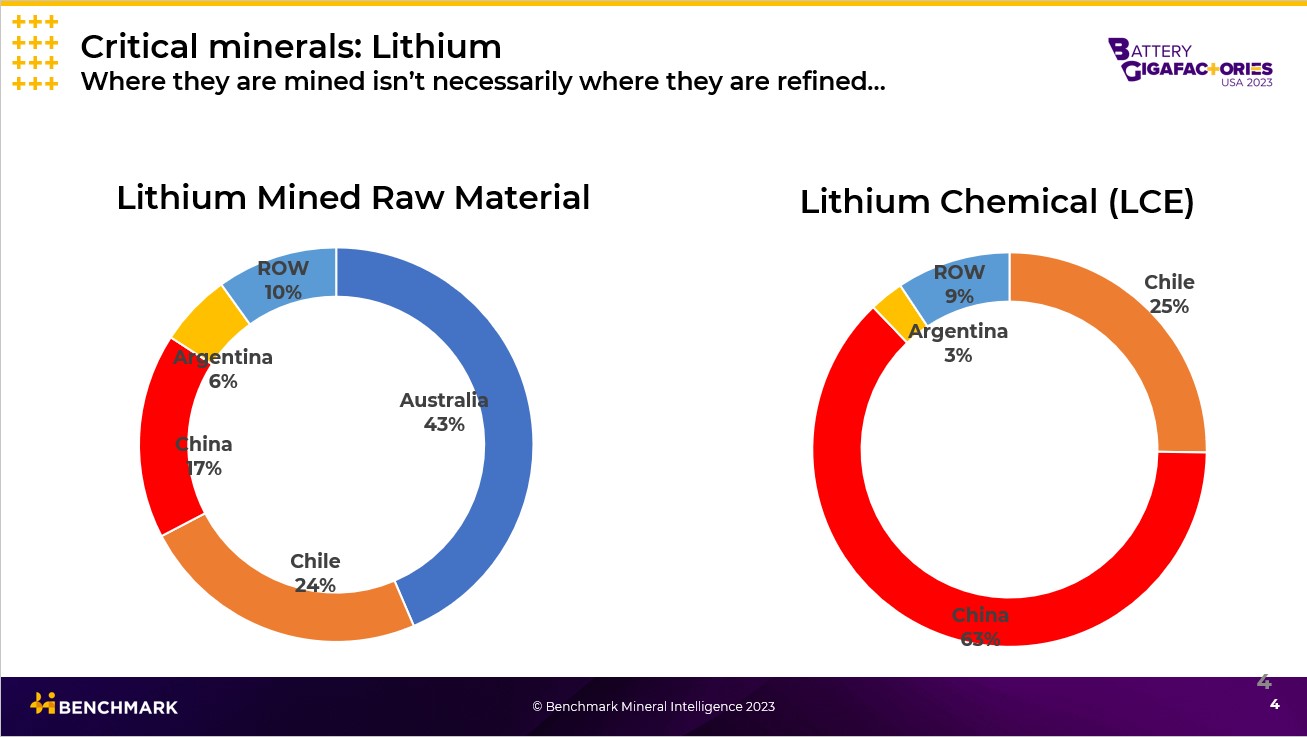

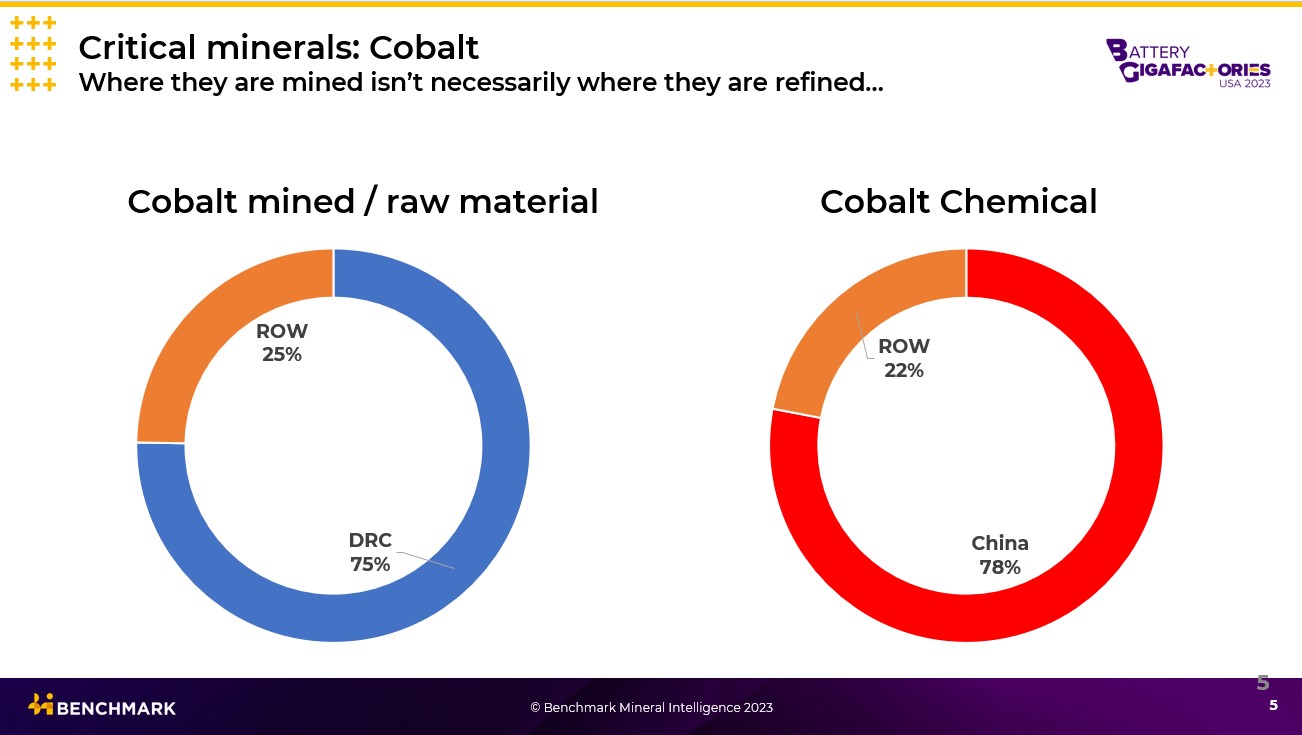

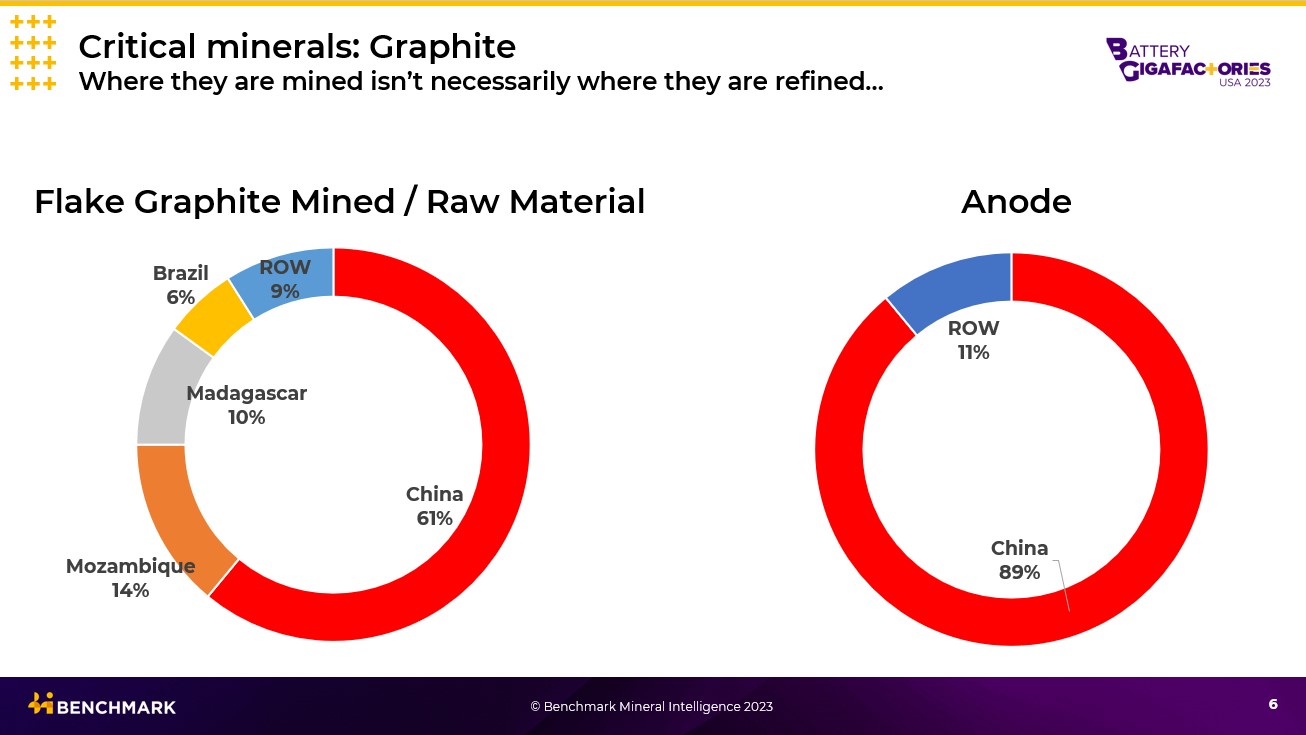

Where these critical minerals are mined aren’t neccsairly where they are refined.

Now, it might sound like an obvious statement, but I really want to underline this because for so many people coming into the industry, it seems like it’s not an obvious statement.

Lithium – 17% of the lithium coming out of the ground was domestically in China, but 63% of lithium is domestically refined in China.

Cobalt is a DRC story but it’s as much a China story. 74% of the cobalt is mined in the DRC, fueled by Chinese investment. But 78% of cobalt is refined in China.

Graphite. 61% is mined in China, it’s an industry that China has both the mining and refining domesticlaly. But actually Chinese companies have been outsourcing htat to countries like Mozambique and Madagascar in recent years. When you have a lock on the flake graphite you have a lock on the anode material.

The crucial thing here for me is building the midstream domestically where you are. Let’s not forget that China produces as many EVs domestically as the rest of the world combined.

The question is how does the US and Europe either strategically decouple from China or work with China, as Chinese companies are the leader here.

Price volatility

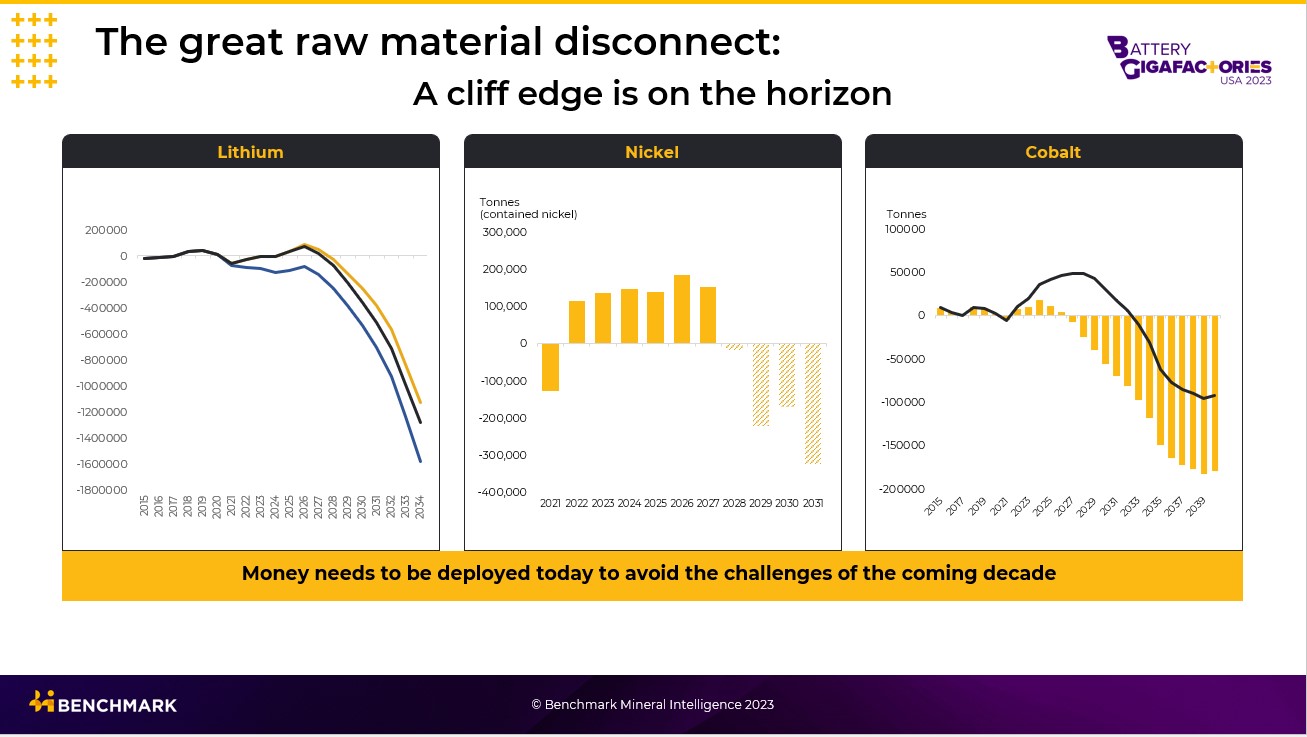

As the critical mineral industries go from the niche to the mainstream, there is simply not enough supply to go round.

Volatility is here to stay.

Volatility of supply and volatility of prices – we’ve seen that in the last number of years.

One of the most important roles Benchmark plays is setting prices for the industry, for you to use in contracts.

It’s a crucial independent tool to bridge this ‘great raw materials disconnect.’ A disconnect where the mine supply is going about half the pace of battery EV demand. And that gap is going to take a long time to bridge, it’s going to take more than this decade to bridge.

$3 trillion opportunity

And how much will it cost?

This is what I want people to mull over. Between now and 2035, $920 billion dollars will be needed to be invested to bridge this great raw material disconnect.

And that’s pretty conservative demand projections from Benchmark. People say we’re too conservative but unless you know what’s happening on the mining side, you cannot predict the scale of the battery and EV side. You have to be completely joined up in your analysis if you’re building infrastructure.

Most of this is mining, $220 billion for raw materials. It’s probably a $3 trillion dollar challenge over the next twenty years to actually build this infrastructure.

The global supply chain base as we know it will still exist yet the US’s strategic decoupling from China, however that looks, will put our industry in the crosshairs.

The response is to build domestic supply chains that sit alongside this global supply chain base.

This makes building mines, chemical plants and gigafactories here – at speed and at scale – of paramount importance regionally and globally.

This is why we are now at the top of the geopolitical agenda, not just here in Washington dc, but worldwide.

This conference will give you the knowledge, the connections and the platform to build a lithium ion economy here in the US.

We are in the midst of a global battery arms race but the US is no longer a bystander.

Yet the very deals done in this room will define this country’s industrial direction for generations to come.

No pressure, thank you very much.

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.