Benchmark shares 7 key takeaways from CESCO Week Santiago

:format(auto):focal(center))

Benchmark is initiating coverage of copper.

We will launch the Benchmark Copper Forecast Service in H2 2024.

Benchmark’s newly established copper team travelled to Santiago, to attend the annual copper industry gathering known as CESCO Week.

Discussions during this year’s event proved to be especially captivating against the backdrop of unprecedented levels of mine disruptions, multi-decade low copper concentrate TC/RCs and surging copper prices. Benchmark’s key takeaways are as follows:

1) A mood of excitement… but also near-term caution

Entering CESCO Week, we expected to be overwhelmed by expressions of bullish conviction at an event that is traditionally dominated by miners. While an outlook of an insurmountable supply gap in the medium to long term became the consensus view, we detected a clear underlying sense of caution for 2024. Notably, market insiders pointed to limited evidence to suggest that the tightness in the concentrate market is percolating through to the refined balance, with sticky Fed policy presenting a further downside risk.

In light of this, many felt that copper prices had run ahead of fundamentals and the macro picture, pointing to the lacklustre pick-up in post-holiday copper demand in China, rising visible inventories, weak premiums, forward curve contango and the breakdown of the inverse relationship with the US dollar. As such, many believed that a temporary price correction is justified until further evidence of refined market tightness emerges in H2 2024.

At Benchmark, we would agree that a small correction is likely following four consecutive weeks of price increase, but, at the same time, we would argue that the broader step-change in prices is here to stay. Benchmark’s view is that the market is already pricing in an outlook beyond the near term, as evidenced by the influx of long positions from large macro and index funds, which are taking a long-term super-cycle view. Benchmark expects downside resistance in the mid-$9,000s/t over the coming weeks, with the prospect of breaching $10,000 on a sustained basis becoming ever more likely, especially as the refined market tightens in H2.

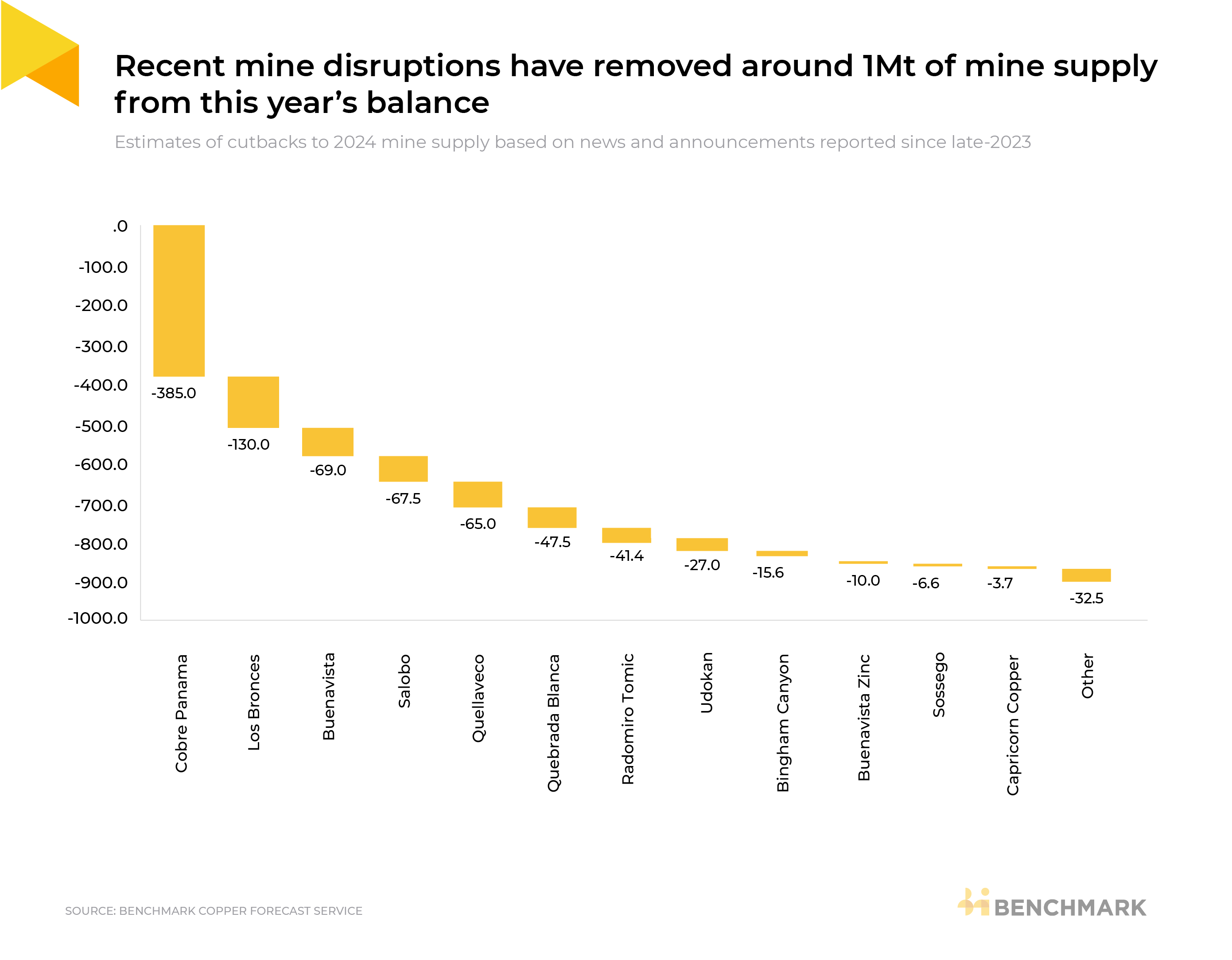

2) Unending risk of elevated mine disruptions

Benchmark has already identified nearly 1Mt of mine supply disruptions due to be realised over the course of 2024, however, the market still sees additional mine supply at risk this year and next. Most notably, initial hopes for a restart of the 400ktpa Cobre Panama mine post-Panamanian elections in May 2024 are quickly fading. A number of market participants that Benchmark spoke with expected the asset to remain on care and maintenance not only this year, but also next year – we share similar sentiment, with current presidential frontrunners unwilling to aggravate persistent and fierce social opposition.

Discussions of supply risks also centred around Zambia and the DRC (close to 4Mt of global mine supply), where low rainfall forced a major power utility in the region to declare force majeure on the supply of electricity to some mines and smelters. Elsewhere, a June copper concentrate export ban hangs over Indonesian miners, which could lead to a 40% production cutback at the 750ktpa Grasberg mine (though consensus expectations are for an extension to be granted until the year-end). Over in Chile, some have cast doubt over Codelco’s ability to recovery from its 25-year production low and achieve its 2024 guidance of 1.325 – 1.390Mt – the company reported production of just 300kt in Q1.

Lastly, the announcements of the suspension of Vale’s 80ktpa Sossego mine in Brazil and Zijin’s 130ktpa COMMUS mine in the DRC mid-CESCO Week added to the sense of mine supply in crisis that permeated the event.

3) Copper conc market takes centre stage, but impact on smelting still unclear

Since the agreement of the annual benchmark TC/RC of $80/8¢ in November, the unprecedented scale of mine disruptions against a backdrop of immense global smelter capacity build-out has suppressed spot TC/RCs at an eyewatering pace. Indeed, Benchmark heard deals quoted at negative TC/RCs last week, with many market participants estimating this year’s deficit at over 500kt, and even more next year.

Where opinions differed, however, was the extent of the announced smelter cutbacks to date: some claimed little evidence of cuts, others saw cuts of more than 500kt, primarily in China. At Benchmark, we tend to agree with the latter view, but only if smelter project commissioning pushbacks are taken into account – cutbacks at operating smelters have so far been very modest in spite of the Copper Smelter Purchasing Team’s (CSPT) unsubstantiated proposal to cut output by 5-10%. We also heard that some of the concentrate shortfall has been offset by increased scrap feed processing, with availability spurred on by higher copper prices.

Overall, the prevailing level of TC/RCs at a time of synchronised maintenance downtime suggests to us that more smelter cuts will be necessary before the year-end, both in China and the rest of world.

4) Future of the concentrate benchmark under question

Amid the reversal of fortunes for smelters, many industry participants began to question the survival of the benchmark system, notably, whether long-term contracts tied to a spot index system will replace the annual benchmark. In Benchmark’s view, while more contracts look likely to be tied to a spot index system next year, the benchmark system is very unlikely to disappear, especially given that many multi-year long-term contracts require a reference benchmark.

Moreover, an annual benchmark allows for more transparent financial planning and is less prone to manipulation. In view of this, speculation was already rife as to where the 2025 benchmark may settle, with most seeing an agreement of around $50/5¢ as fair, taking cues from past benchmarks and smelters’ breakeven costs. Antofagasta’s mid-year contract negotiations with smelters, which start next month, should give us more clues on the outlook – Benchmark will be monitoring this closely.

5) A sense of nervousness on the refined market outlook for 2024

In stark contrast to the concentrate market, many market participants sensed that the refined copper market is yet to show convincing evidence of tightness, especially in China, where smelters were rumoured to be planning to export some stock last week. In Benchmark’s view, this is largely attributed to reduced spot purchases by Chinese semis fabricators, who are highly price-sensitive in the short term, in conjunction with a refined metal stock buffer created by strong Chinese refinery output in 2023 and Q1. With overall end-use demand across the world improving and Chinese smelters embarking on a period of well above-normal maintenance shutdowns this quarter, Benchmark foresees the refined market tightening markedly into the second half of this year.

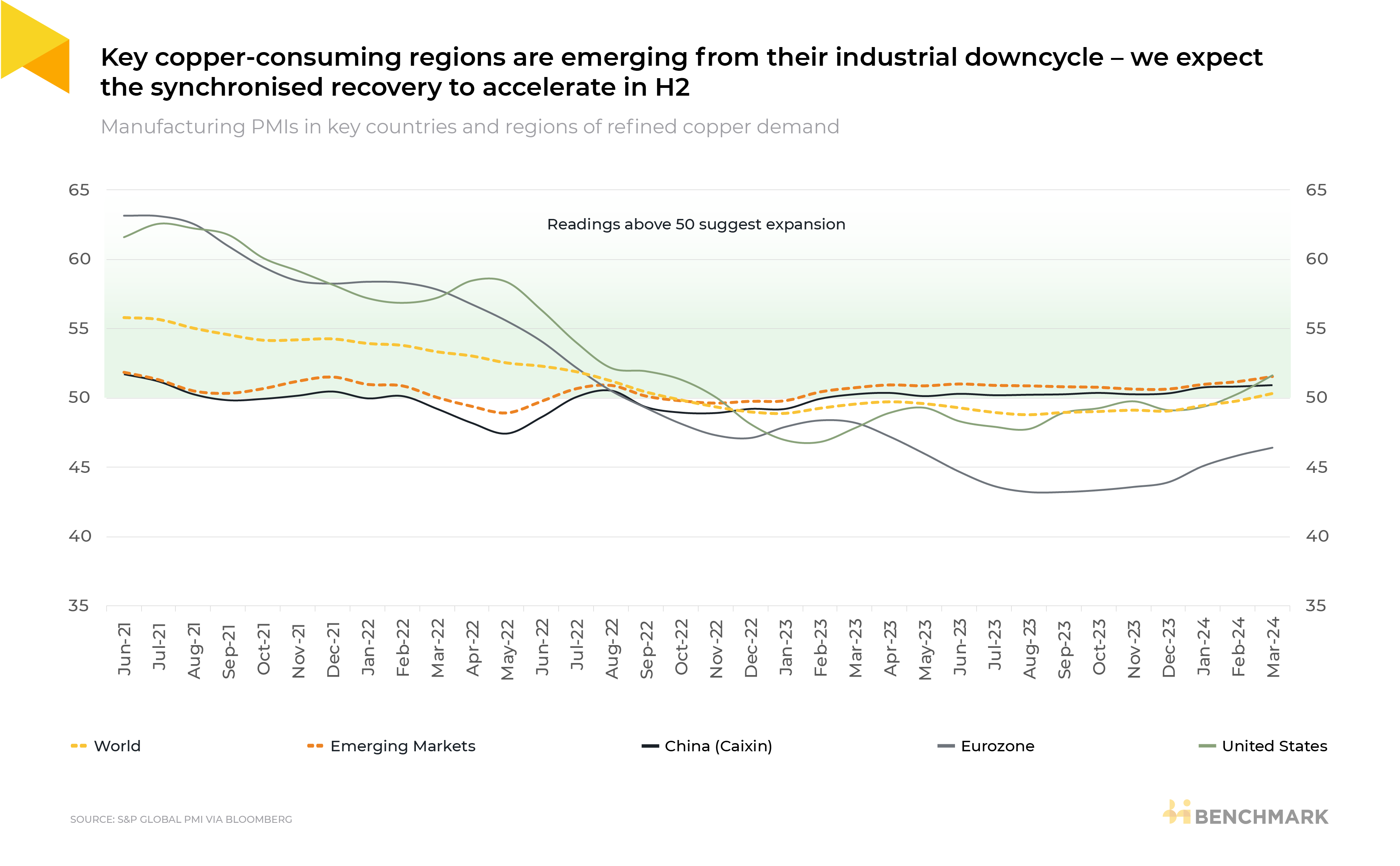

On the end-use demand front in China, while housing completions have declined sharply in Q1, Benchmark sees weakness in the construction segment being more than offset by strong consumption from the grid and new energy segments, especially in H2, as local governments catch up on their investment targets. Overall, while China’s demand growth is expected to moderate from last year’s level, most market participants that we spoke with still expected a healthy 2-4% y/y increase this year. Outside of China, Europe and the US appear to be emerging out of their industrial downcycle, as evidenced by improving PMI figures (shown below), and will help to drive synchronised demand growth in H2, accelerating further into 2025. Overall, global demand growth of 2-3% y/y in 2024 seems to represent consensus, with the refined market tightening markedly in the second half of this year and moving into more pronounced deficit into 2025 as supply shortages continue to bite.

6) Long-term demand destruction looks inevitable

There appeared to be a growing realisation that the copper market is finally face-to-face with the long-anticipated structural supply gap, which is no longer theoretical. The recent mine disruptions have effectively fast-tracked the transition to deficit, eradicating the previously forecasted two- to three-year surplus buffer. In such an environment, copper thrift and substitution are inevitable, especially in new energy transition segments, where research and development is advancing at lightning pace and easy gains are more likely to be made than in more mature end-use markets.

Benchmark will be diving into these segments at great depth, utilising our in-house technological expertise to move away from demand forecasts based around static intensity assumptions.

7) Demand from data centres – more noise than substance

Of course, we couldn’t end this piece without mentioning prospects for copper demand from datacentres – a subject that had blown up in coverage in the run-up to CESCO Week. Whilst we heard copper intensity assumptions being quoted anywhere from 10kt per GW to 100+kt per GW, Benchmark’s key takeaway is that robust, defensible numbers are lacking and we will need to run our own analysis on the subject – watch this space!

If you would like to hear more about Benchmark’s upcoming copper forecast service, or indeed like to sign up to the Copper Weekly, please fill in the form below:

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.