Can Africa fill the EU’s critical mineral deficit?

:format(auto):focal(center))

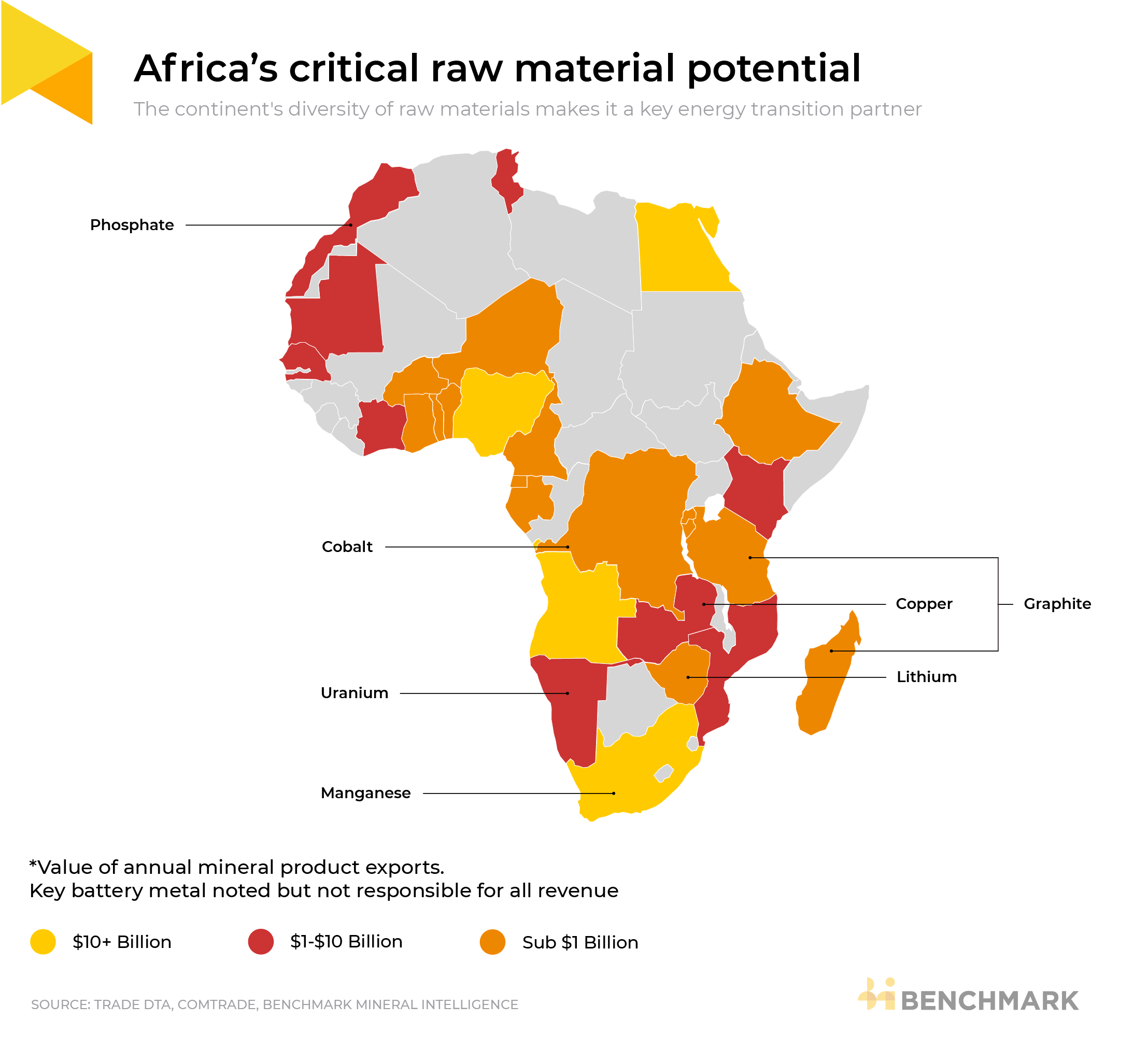

Since the Critical Raw Materials Act (CRMA) established ambitious targets for the EU to strengthen the autonomy of its critical raw material supply chains and reduce dependence on China, the diversity of Africa’s minerals has seen the EU prioritise the continent as a key energy transition partner.

Africa is currently a leading exporter of at least 10 critical minerals to the EU and European policymakers have signed several Strategic Partnerships post-CRMA to enhance cooperation with mineral-rich countries across the continent. These partnerships are designed to integrate critical mineral value chains and promote economic development, while upholding the EU’s rigorous sustainability standards.

Africa currently accounts for 78% of global cobalt supply, 19% of flake graphite supply, and 4% of lithium supply, according to Benchmark data.

Through its Global Gateway Initiative (launched in October 2021) the EU is also attempting to regain lost geopolitical influence in the region. Counterbalancing China’s Belt and Road Initiative by promoting European investment in infrastructure projects throughout the continent.

DRC underpins Europe’s battery ambitions

Across the spectrum of battery materials, cobalt is forecast to experience the largest supply shortfall in Europe by the end of the decade.

“Mined cobalt output in the EU currently accounts for less than 1% of total global supply. Europe produces about 10% of the world’s refined cobalt, leaving it reliant on imports of cobalt intermediates from outside the region,” said Will Talbot, cobalt analyst at Benchmark.

This reliance is only set to increase over the short-to-medium term as the bloc ramps up refining capacity to meet the CRMA’s 40% processing target by 2030. Benchmark’s Cobalt Forecast shows that cobalt extracted in the EU will be equivalent to only 2% of the bloc’s battery demand by the end of decade.

With this forthcoming supply deficit in mind, the EU has partnered with the cobalt-rich Democratic Republic of Congo (DRC) and neighbour Zambia, signing provisional critical raw materials agreements with the two countries in October 2023.

As well as accounting for more than two-thirds of global cobalt production out to 2030, the DRC also has considerable reserves of lithium that could meet up to 10% of the EU’s lithium demand by 2035.

The bloc has agreed similar partnerships with Namibia (November 2022) and Rwanda (February 2024). Although its partnership with Rwanda has drawn sharp criticism from Congolese lawmakers due to the former’s alleged support for M23 rebels in eastern DRC – a potential sticking point as the EU seeks to progress its agreement with the DRC.

Breaking China’s grip in Africa

Chinese firms currently have financial stakes in 18 of the 26 cobalt-producing assets in the DRC and 80% of lithium mines across Africa. By establishing Strategic Partnerships, the EU hopes to stimulate private investment in Africa’s mining sector and associated infrastructure to develop alternative critical mineral supplies and trade routes for Western allies.

The EU’s partnership with the DRC and Zambia includes a commitment, alongside the United States and other regional actors such as Trafigura, to support the development of the Lobito Corridor; a proposed upgrade to the existing railway connecting the Angolan port of Lobito with Kolwezi in the DRC. An expansion into Zambia is also planned.

“The Lobito Corridor is an illustration of the EU’s and the US’s ambition to counter China’s geopolitical involvement in the African Copperbelt, and, at the same time, it is a way for both to diversify supply. Both hope that more of the DRC’s minerals will be shipped to Western players through the refurbishment of the railway,” said Bryan Bille, policy analyst at Benchmark.

Pilot shipments indicate that transporting raw materials from the copper belt via the Lobito Railway could cut transportation times to port by more than a third. Shipping from the Atlantic coast would also considerably reduce transit times for minerals destined for Europe and North America markets.

“However, it remains to be seen in practice if Chinese players will also use this corridor. There might be a gap between geopolitical aspirations and eventual practical implications,” Bille added.

Benchmark’s upcoming webinar will be the first instalment of our quarterly webinar series focused on the impact of geopolitics and government legislation on the supply chain.

For further insight, join our webinar on Thursday 28 March at 15:00 (GMT): How Election Year Will Shape Critical Mineral Supply Chains.

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.