China’s latest rare earths quota could sustain weak prices

China’s latest rare earth quota has raised the total output limit for 2023 by around 14% over 2022, a move that could entrench low rare earth ore and oxide prices.

“This 14% year-on-year growth in the quota is quite significant and will ensure that the market is well-supplied,” said Benchmark project manager Daan de Jonge.

Supply is the biggest downward pressure on rare earths prices at the moment although weak downstream demand is also contributing.

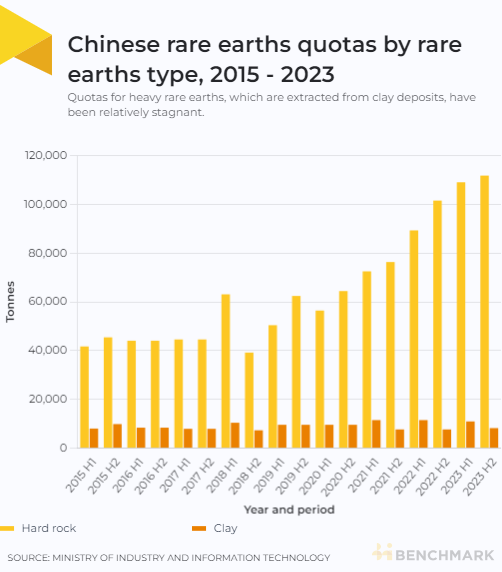

The latest quota, released on 25 September, limited total production from four major producers to 120,000 tonnes and 115,000 tonnes of mined and refined material respectively. It applies to output for the remainder of 2023.

The four entities subject to the quota operate all of China’s legal domestic mines and the majority of its refining capacity.

China’s Ministry of Industry and Information Technology and the Ministry of Natural Resources issue rare earth quotas twice each year. The last quota, released in March, had set output for the first half of the year to 120, 000 tonnes and 115, 000 tonnes for mined and refined material respectively.

Although the quota figures were the same in March and September, their combined total marks an overall growth on last year’s output limits.

China’s output is a major determinant of rare earths prices thanks to its share of global supply, which is forecast to be around 71% in mined praseodymium-neodymium (PrND) and 86% in PrNd oxides in 2023, according to Benchmark data.

Consecutive quotas increases by the Chinese government have been a significant driver of overall rare earths price declines since reaching near-historic peaks in early 2022.

Further pressuring prices, this recent oversupply from China has coincided with weak downstream demand over 2023 from both wind and EVs, the two biggest rare earths end consumers.

The latest quota increase from China should sustain lower prices, primarily for the light rare earths.

The four companies allocated the quotas were China Rare Earth Group, China Northern Rare Earth Group, Xiamen Tungsten, Guangdong Rare Earth Industry Group.

Together, the two rare earth mining and smelting quotas issued for 2023 totaled 240,000 tons and 230,000 tonnes respectively.

China’s pursuit of ‘rational prices’

The ongoing price decline for rare earths supports the Chinese government’s objective to lower their market value and achieve what it calls ‘rational prices’.

The government believes the rare earths price rally over the early 2020s were preventing China’s industry, in particular its growing EV industry, from accessing raw materials at reasonable cost.

“For China, rational prices are ones where the growth is possible across the entire supply chain, from mining to EV manufacturing. Ensuring new capacity is a reasonable investment while maintaining stable input prices for REPM and motor manufacturers is a major objective for China’s MIIT,” explained de Jonge.

Impact on Western capacity building

China’s concern to achieve lower prices stems from the fact that it presides over a well-developed domestic rare earths supply chain, spanning mines to magnet-making.

By contrast, low prices run counter to the interests of the Western governments and producers, whose primary concern as they begin domestic rare earths buildout is developing its upstream.

“Western miners tend to require higher prices for most investors to take action. This is due to higher cost positions and greater return-on-investment (ROI) targets. In the absence of high prices, it is difficult to ascertain what realistic ROI targets would be in the current market given the persistent uncertainty surrounding longer term price growth,” explained de Jonge.

The few operating Western rare earths miners have been struggling to maintain cost efficiency under current market conditions.

Average selling prices per kilogram of material fell 51% year-on-year at US company MP Materials in its quarter two results this year while in August, Australia’s Lynas reported a 51% quarter-on-quarter dip in realised prices.

This impact of China’s output on Western rare earths mining viability shows the sheer extent of its dominance in this market, as movements within its industry are set to shape even the pace at which other regions can build independent capacity.

Benchmark’s Rare Earths Forecast examines supply, demand, prices and costs for rare earth elements out to 2040 with full updates every quarter.

To learn more about this service and to speak to our team, please provide your details here and our team will get back in touch.

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.