Going local: sourcing rare earths for wind energy from regional supply chains

:format(auto):focal(center))

The increasingly ambitious wind energy targets being set to reduce reliance on traditional energy sources – both in terms of geographical and material dependence – present a challenge from a supply chain perspective. This is particularly true for rare earth elements (REEs), with top policymakers increasingly calling for de-risked supply chains.

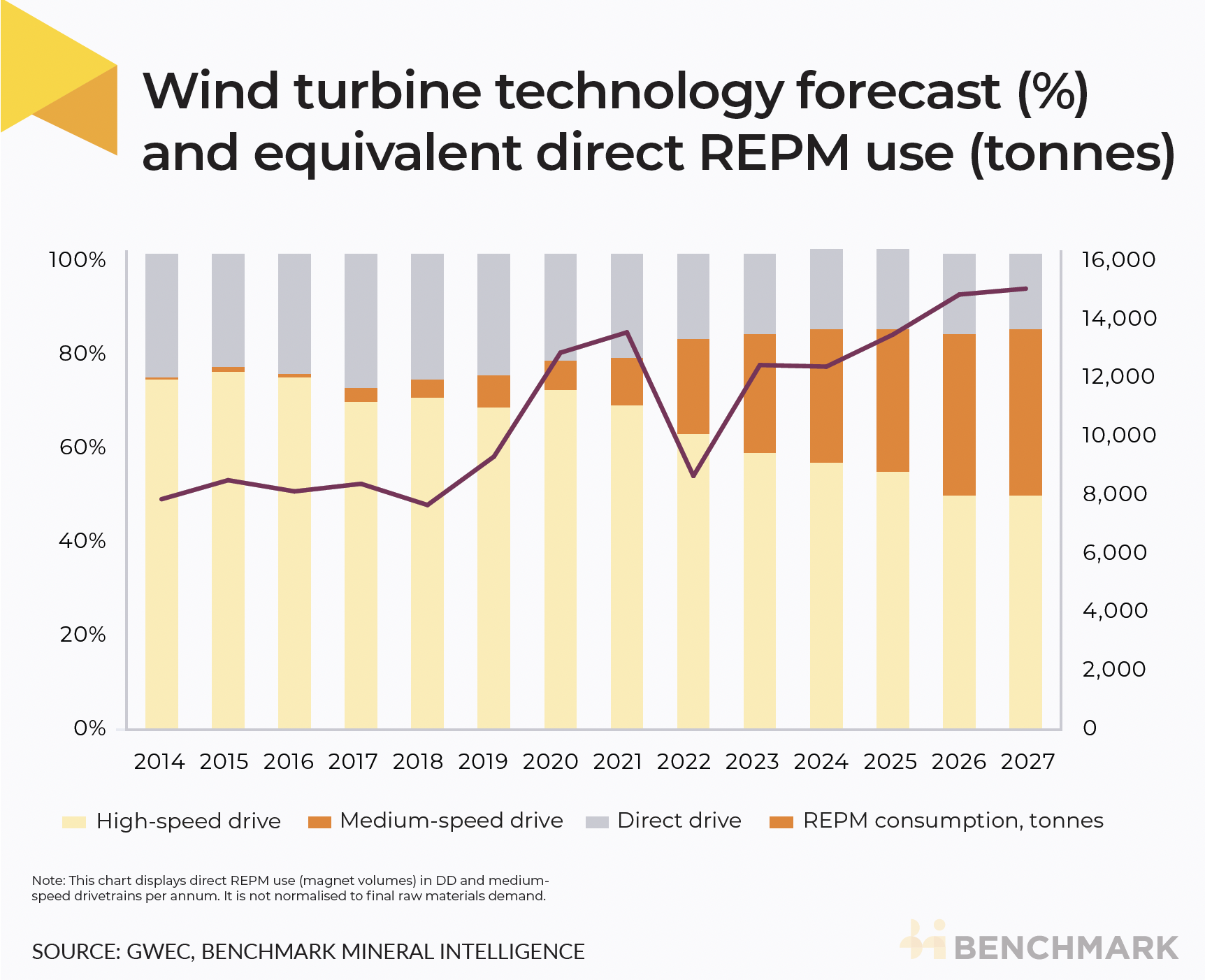

Wind energy uses large amounts of rare earth permanent magnets (REPMs), contributing significantly to global demand. Wind energy OEMs have faced challenges in obtaining the quantities of REPMs they need, despite supply growing at record speed and demand softening thanks to ‘hybrid’ wind energy technologies increasingly replacing standard direct drive (DD) turbines over the past five years. Hybrid systems (medium-speed drivetrains) use just one-tenth of the REPMs needed in a DD drivetrain.

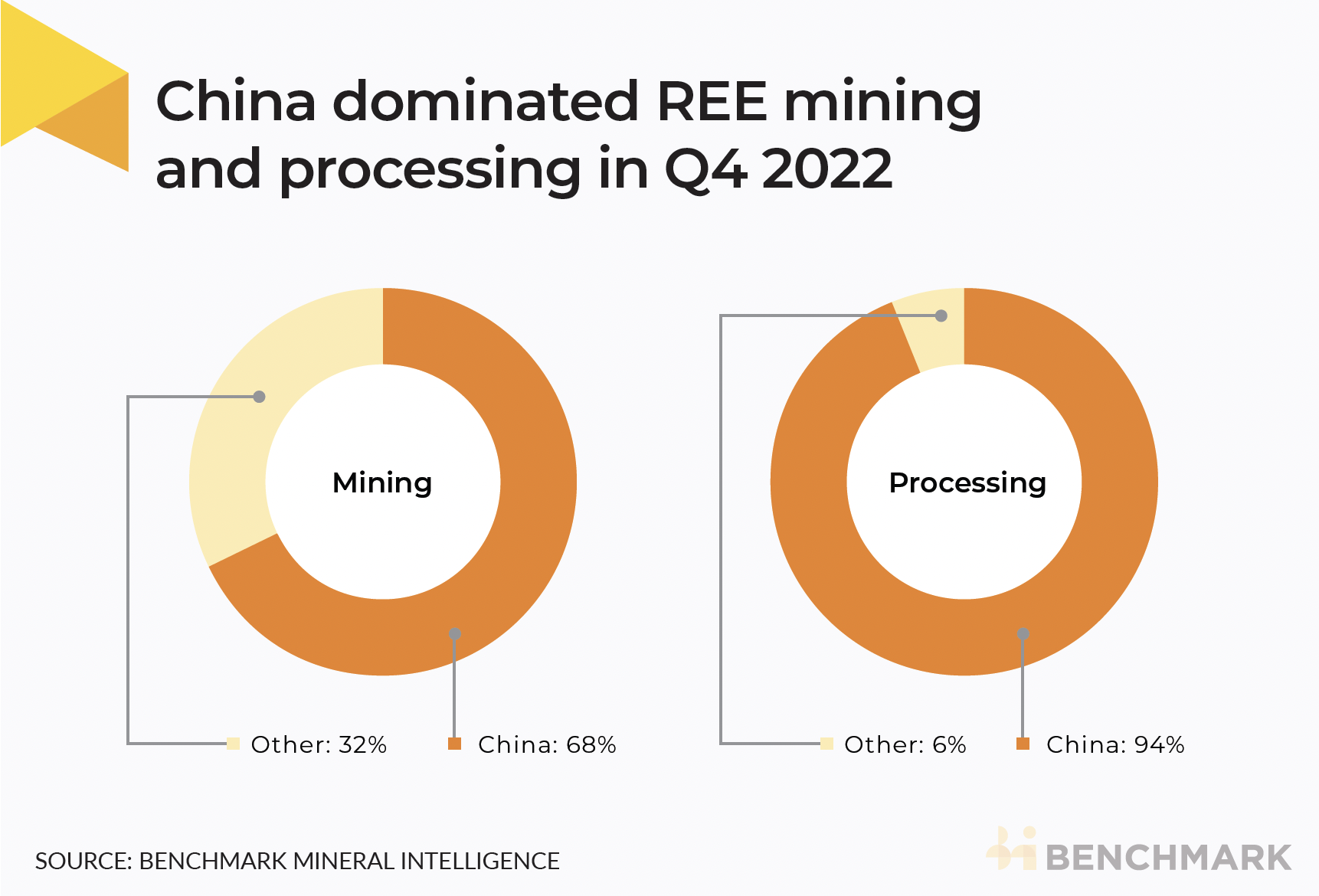

In the fourth quarter of 2022, China accounted for 68% of rare earth mining and 94% of downstream processing. Only a meagre amount of materials was processed elsewhere, principally in Malaysia and Estonia.

Because the wind industry is exposed to the impacts of geopolitical tensions – and following a toughening of China’s export restrictions of rare earth-related technologies – there is growing policy and industrial concern in Europe, North America, Australia and elsewhere.

While sourcing enough REPMs for wind energy generation can be difficult, the greatest challenge for the industry is being able to source them domestically or from a de-risked supply chain. In major markets such as Europe, the US and Australia, demand for REPMs in wind energy is substantially larger than local supply.

Policymakers have made some efforts to bridge this gap, for example in the US, the UK and Australia, where Benchmark expects to see rapid processing capacity growth by 2024-2025:

While the pipeline of processing facilities in North America, Australia and Europe is significant, it will take time for the first inputs to be converted into saleable material, and to fund and construct the required facilities.

The availability of locally processed and manufactured REPMs may be further limited, in the short and medium term, by offtakes securing sizable portions of planned production for EV manufacturers. Whereas a facility such as Solvay’s La Rochelle, in France, may be able to scale up fast thanks to existing knowledge and experience, other parts of the puzzle need to align. Before a diversified, de-risked and sizable local supply chain is established, more than 300 GW of additional wind power capacity may already have been built.

Benchmark forecasts a more diversified and regionally scaled rare earth processing market beginning to take shape after 2025, particularly in Europe, North America and Australia.

Environmental protections and economic concerns, such as high capex requirements and low Chinese costs, together with considerable project lead times, cast a shadow on capacity addition forecasts, however. A large part of the wind industry will, as a result, have to rely on sourcing REPMs from China in order to meet clean energy demand in the short term.

This Benchmark analysis was also published in the Global Wind Energy Council’s Global Wind Report 2023.

Benchmark is launching a new Rare Earths Forecast to provide a detailed long term outlook for supply, demand, prices and costs for rare earth elements (REEs).

If you and your colleagues would like to speak to our team for more on this service, please provide your details here and we’ll contact you shortly.

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.