Lithium prices hit record high as market pricing takes hold – 2022 in review

:format(auto):focal(center))

2022 was the year when market-led contracting mechanisms took hold in the lithium market.

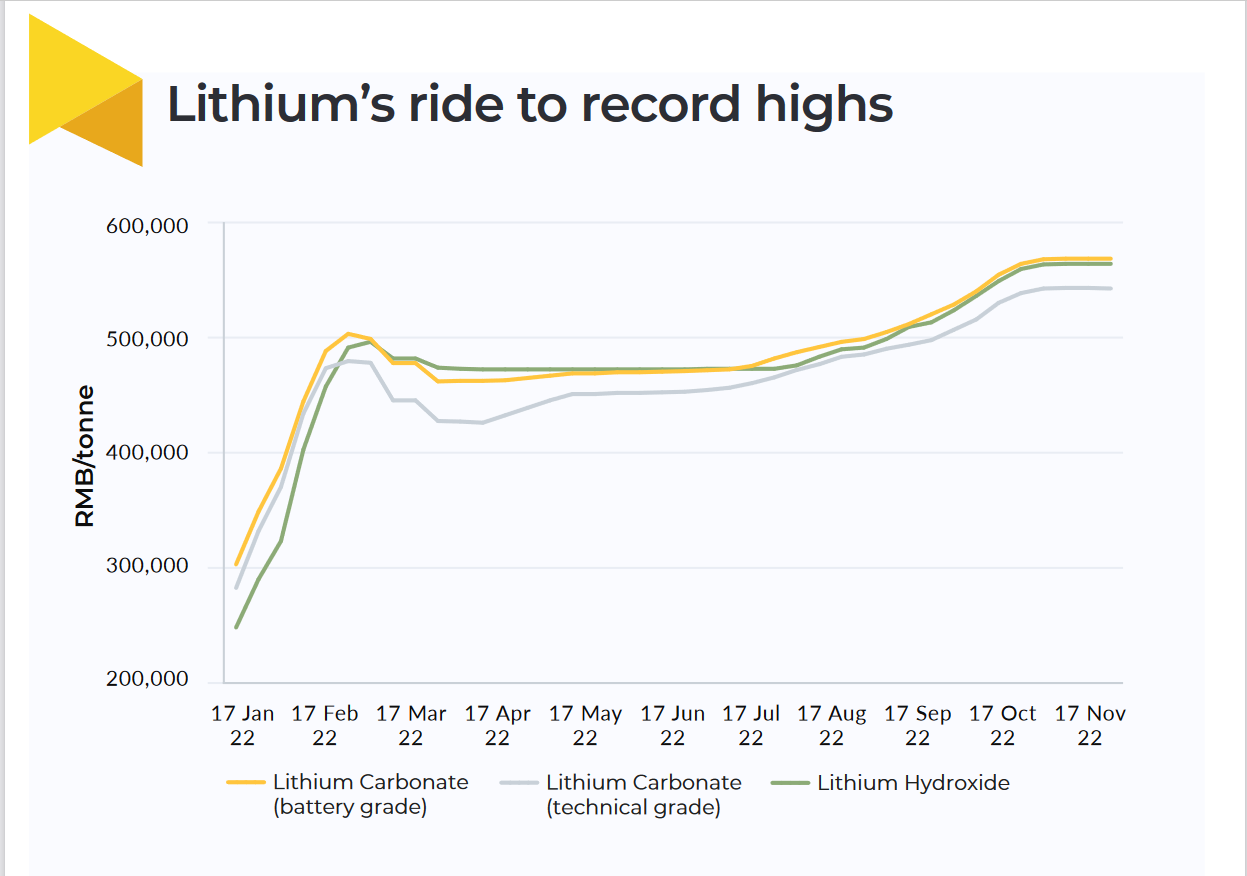

The first quarter of 2022 saw a record-breaking price rally in the Chinese domestic lithium market, with battery grade lithium carbonate soaring by 101.4% between January and March, as a result of a widening supply deficit.

Lithium hydroxide followed this trend, driven by similar fears over tightness in the structurally smaller hydroxide chemical market.

However carbonate held a price premium over the former throughout the first quarter on the back of rising downstream demand from lithium iron phosphate (LFP) cathode manufacturers.

Meanwhile in the international market, the first quarter also saw a strong upward revision in pricing for lithium chemical volumes delivered under supply contracts. This came as a result of a shift in late 2021 towards producers restructuring contracting mechanisms to contain more frequent price breaks, in a bid to move sales towards more market-led pricing.

By February, pricing in the international spot market reached near parity with the domestic market in China, which typically acts as a bellwether for international trading, as a result of the lagged impact of the Chinese price rally on ex-China sentiment.

Particularly in Europe and North America, spot market pricing for small volumes of lithium hydroxide rose sharply in the first quarter, in response to tightening availability amid Russia’s invasion of Ukraine. This saw Russian hydroxide volumes being severely restricted for delivery into Europe due to trade and transport sanctions.

Towards the end of the first quarter, the price rally in the Chinese domestic market began to decelerate on the back of market participants’ hesitance to surpass the RMB 500,000/tonne price threshold, with this stability compounded by comments from Chinese government ministries that pricing should be encouraged back down to more normalised levels.

A subdued second quarter

The second quarter started with a quieter period of activity in the Chinese domestic market and temporary softening of prices, on the back of localised Covid-19 restrictions, particularly in Shanghai, halting or severely limiting operations for many automakers and consequently weighing on downstream demand.

Meanwhile in the international market, activity was also subdued, as is typical in Europe and North America during the summer months. However, this illiquidity was exacerbated by consumers employing a cautious watch-and-wait strategy before purchasing material whilst virus developments in China played out.

Following the easing of Covid-19 restrictions in Shanghai in early June, market activity in the Chinese domestic market recovered.

Seasonal domestic supply from Qinghai brine projects, coupled with uncertainly over whether tighter virus restrictions would return, meant pricing for both carbonate and hydroxide remained relatively stable throughout June and July, however.

Demand recovers

As demand from downstream cathode and cell manufacturers began to recover towards the end of the third quarter, prices for lithium chemicals in the Chinese domestic market began another rally, with increasing feedstock prices, particularly for spodumene from Australia, squeezing converter margins.

In Japan and South Korea, demand remained robust throughout this period, with spot market pricing surpassing domestic China pricing, as consumers competed for any available volumes.

During this time, pricing for spodumene concentrate also increased dramatically, with feedstock availability increasingly becoming a focal bottleneck in the market.

As a result of many spodumene contracts being directly tied to the rallying lithium chemicals market, Benchmark saw concentrate prices rising by 113.7% from January to November 2022.

Additionally, the smaller volumes sold in Pilbara Minerals’ BMX auctions, whilst not wholly representative of the prevailing market price, settled at multiple record highs throughout the year, clearly indicating the extreme supply tightness.

Nonetheless, lithium chemical market activity outside of Asia remained stymied through the second half of 2022, as non-battery consumers showed resistance to paying such high prices for lithium products, amid rising costs for other raw materials and energy.

As Chinese automakers looked to accelerate production rates into the fourth quarter of 2022, to boost sales ahead of the discontinuation of China’s electric vehicle subsidies on 1 January 2023, the domestic price rally was supported before tightening Covid-19 restrictions once again saw pricing level off towards the beginning of December.

As such, prices for battery grade carbonate climbed by 20.8% from the end of July through to the start of December, with hydroxide pricing increasing by 19.5% in the same period, both recording fresh highs of over RMB 575,000/tonne ($82,225).

Following the price rally at the beginning of the fourth quarter, prices in the Chinese domestic market began to stabilise, then soften marginally, in early December on the back of cathode manufacturers adopting a watch-and-wait strategy towards purchasing material amid the Covid-19 disruptions in China. Cathode producers instead worked through raw material inventories built up throughout November.

Despite Covid-19 restrictions being eased in the second week of December, uncertainty still remained with mixed signals from the market regarding the demand picture for the final few weeks of 2022 and ahead of 2023’s notably early Spring Festival in China.

Tony Alderson is an analyst at Benchmark.

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.