What the EU’s new corporate sustainability directive means for the battery supply chain

:format(auto):focal(center))

Approved by the Council of the European Union (EU) in May, the Corporate Sustainability Due Diligence Directive (CSDDD) entered into force in July, impacting battery supply chain players that operate in the EU.

The directive aims to foster sustainable and responsible corporate behaviour in companies’ operations and across their global value chains.

As this legislation is a directive, member states have some room for manoeuvre in how they implement it domestically, though ultimately the CSDDD intends to harmonise due diligence policies across Europe.

“EU battery supply chain players should prepare for the CSDDD to meet impending legal requirements, manage reputational risk, and appeal to socially responsible investors,” said Soad Chambazi, a sustainability analyst at Benchmark.

The United Nations Guiding Principles on Business and Human Rights (UNGP) was used as a reference point for drafting the CSDDD. Only nine of the 21 EU-based active mining and refining companies tracked by Benchmark across its Sustainability Indexes have stated they implement these principles, Benchmark data shows.

Key points

1) What are the mandates of the Corporate Sustainability Due Diligence Directive?

The directive requires companies to implement a due diligence process that assesses the environmental and human rights impacts of their operations as well those of their business partners up and downstream of them in the supply chain.

The CSDDD goes beyond reporting and requires companies take measures to prevent environmental harm or human rights abuses. Additionally, companies can be held liable for the damage caused and will have to provide full compensation.

One of the more specific aspects of the directive is that companies must establish clear communication channels with stakeholders relevant to their operations and a complaints platform providing individuals and organisations with direct access to the company.

Companies affected by the directive are also required to adopt a climate transition plan in line with the Paris Agreement on climate change.

2) Who is going to be affected?

There are two categories of companies affected by the directive.

The first is EU registered companies with more than 1,000 employees and a net turnover of more than €450 million ($492 million) worldwide. This also applies to EU registered companies with franchise or licensing agreements and more than €22.5 million ($24 million) in royalties and €80 million ($88 million) net turnover worldwide in the past two consecutive years.

The second is for non-EU registered companies with more than €450 million ($492 million) net turnover in the EU. The employee threshold is not applicable here and the same is true for franchising and licensing agreements.

Though the proposed rules do not cover micro-companies and SMEs, such enterprises could be indirectly affected as business partners in value chains.

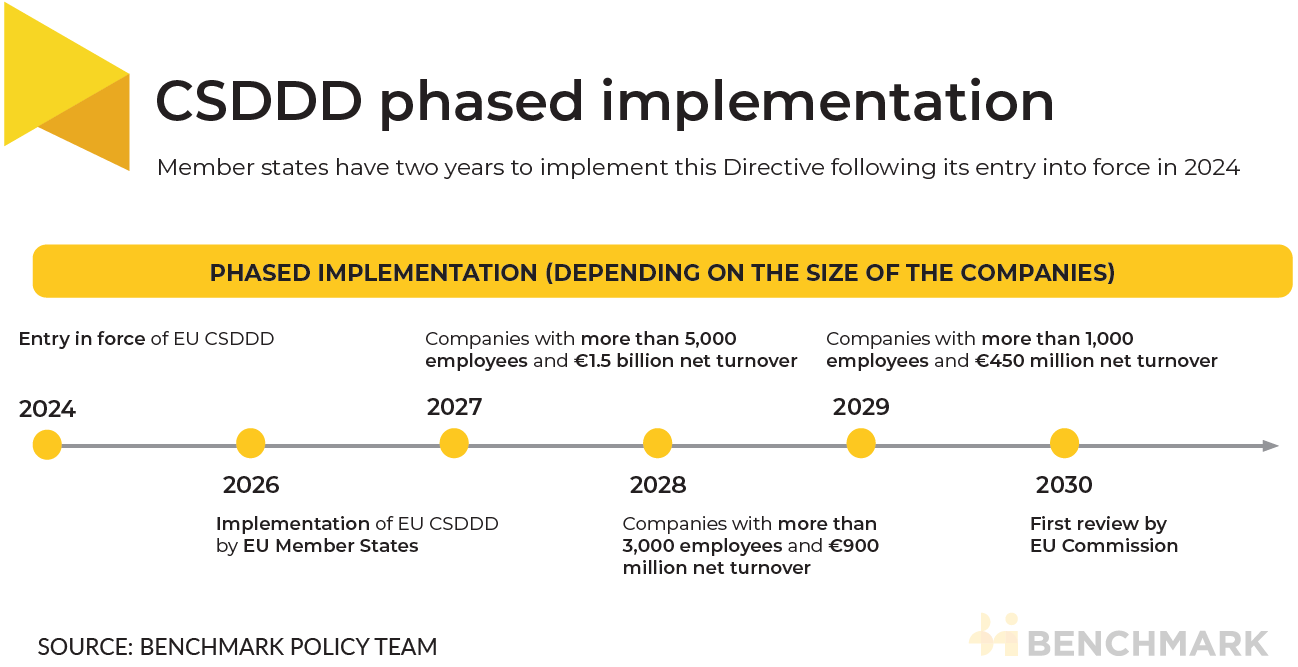

3) When are companies expected to start reporting?

The directive entered into force on 25 July 2024 and by 2026 member states are required to implement the directive into national regulation. This takes the form of the laws, regulations, and administrative provisions necessary to comply with the directive.

By 2027, the CSDDD measures will apply to companies with more than 5,000 employees and a net global turnover of more than €1.5 billion ($1.6 billion). These criteria become more stringent – lowering the number of employees and net global turnover – until 2029 when the targets will apply to all companies stipulated in the directive.

4) What are the repercussions in the case of noncompliance?

Individuals and civil society organisations can receive full compensation from companies who have not met their due diligence obligations.

There are also financial sanctions accounted for in the CSDDD where member states should apply a minimum penalty of 5% of the company’s worldwide net turnover for the previous financial year.

5) How can companies prepare for the CSDDD?

The policy makers who formulated the CSDDD used the United Nations Guiding Principles on Business and Human Rights (UNGP), as a point of reference. Though voluntary, the UNGP is a fully developed framework meaning companies can implement its policies and management systems now and cover most of the topics required under CSDDD as a result.

According to Benchmark’s Sustainability Index data, 19 of the 35 critical battery mineral mining and refining companies with active operations in the EU have stated UNGP implementation.

Learn more about Benchmark’s ESG services, including how we can carry out a bespoke lifecycle assessment for your company’s operations, by filling out the form below:

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.