What’s going on with lithium prices?

:format(auto):focal(center))

Lithium prices have recently ticked down in the Chinese spot market, ahead of the Chinese lunar new year this month.

This has led to fears about a market downturn and a significant change in the direction of lithium prices. Battery-grade lithium carbonate prices fell by 6% in December in Renminbi, according to Benchmark.

Despite this change in direction, here are five reasons why the lithium market is likely to remain tightly balanced between supply and demand this year.

1. Contract prices will continue to move upwards.

Prices for battery-grade lithium in China doubled in 2022 to RMB 536,000 ($78,135) a tonne. Older lithium supply contracts are still being renegotiated to reflect recent market price moves, meaning that recent high lithium prices may still not be reflected in the prices that cathode producers and battery makers are paying today. Some contracts still lag spot market prices by up to six months. As they are renegotiated, producers will try to remove previous floor and ceiling price conditions and increase the frequency of pricing breaks, leading contract prices to more quickly catch up to spot market prices.

2. Spodumene prices are still rising.

Prices for spodumene lithium feedstock are still increasing. Australian lithium miner Pilbara Minerals announced that its contracts for 2023 have been revised upwards to an average of $6,300 a tonne CIF. Contacts have reported to Benchmark that other contract renegotiations have been completed, shifting up prices.

Prices for spodumene rose by 167% in 2022 and 8% in December, according to Benchmark, to $6,401 a tonne. Benchmark anticipates that the ongoing renegotiation of spodumene offtake contracts will see feedstock prices continue to rise through the first quarter. That will pressure margins at converters, who in turn may raise lithium chemical prices after the Chinese New Year. There is a lag between when lithium is mined and shipped from Australia to when it is turned into a battery-grade chemical. In addition, for automakers the impact of lithium prices is not felt until about six to nine months after lithium is first mined, or sometimes longer.

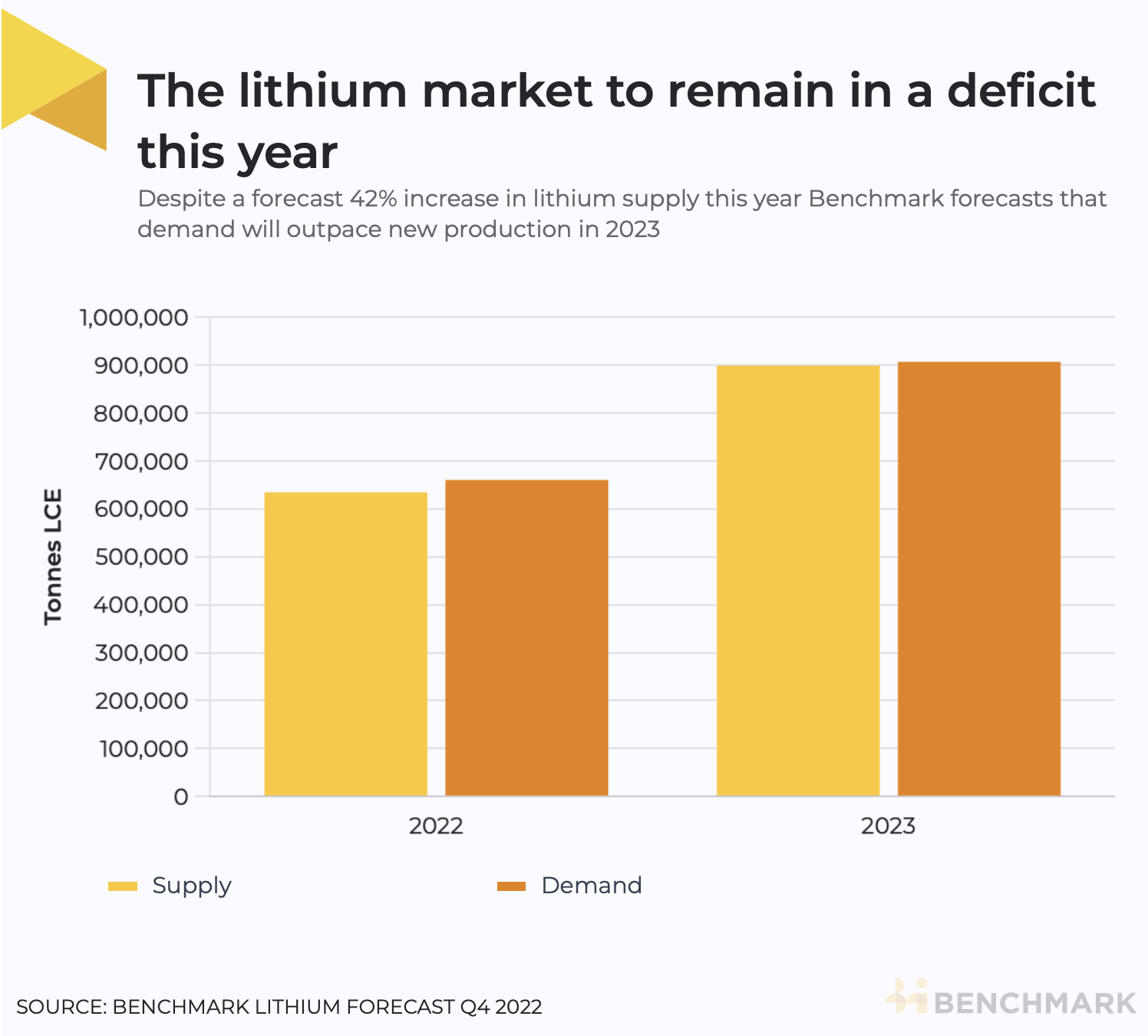

3. New supply in 2023 will take time to come to the market.

This year, mined lithium supply is set to increase by 42% from last year, according to Benchmark, driven by expansions at existing mines in Australia and Chile as well as new projects coming into production. Yet lithium supply growth remains limited in the short term, with the market not expected to be balanced between supply and demand until 2025. New greenfield projects such as the Mt Holland mine in Australia, the Cauchari-Olaroz brine project in Argentina, Sigma Lithium’s project in Brazil, and North American Lithium in Canada, will all take time to come to full production. Converting these units to battery-grade lithium chemicals may take even longer.

4. Chinese lithium will be high-cost.

Chinese companies announced investments of $5.4 billion in domestic lithium resources in the fourth quarter, most of it in Jiangxi province. Supply from domestic lepidolite mines is forecast to rise by 69% this year from 2022. But China’s domestic lepidolite reserves are very low-grade and higher-cost. In addition new projects globally face higher costs due to rising equipment and labour costs. As a result lithium prices are unlikely to go back to where they were in 2019 as long term incentive prices have moved higher.

5. Demand outlook remains robust.

China is currently grappling with the consequences of the sudden reversal of President Xi Jinping’s “Zero-Covid” policy, as the virus spreads around the country. A seasonal slow down in electric vehicle sales is expected as Chinese EV subsidies are also removed this month. Yet demand could rebound once the situation settles down. In addition, electric vehicle purchase tax credit incentives in the US in the Inflation Reduction Act could boost sales in the country. Benchmark forecasts that lithium demand will rise to over 900,000 tonnes LCE in 2023 from just over 600,000 tonnes in 2022.

Benchmark’s Lithium Forecast service provides a comprehensive view of lithium supply, demand, prices and costs out 2040 which is fully-updated every quarter. Speak to our team for more information on the service.

And join us on Thursday 2 March for our webinar – Lithium: The Multi-Billion Dollar Question. Please register with your business email here.

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.