Battery raw material prices on the rise again after overbuying wiped out 2021–23 gains

:format(auto):focal(center))

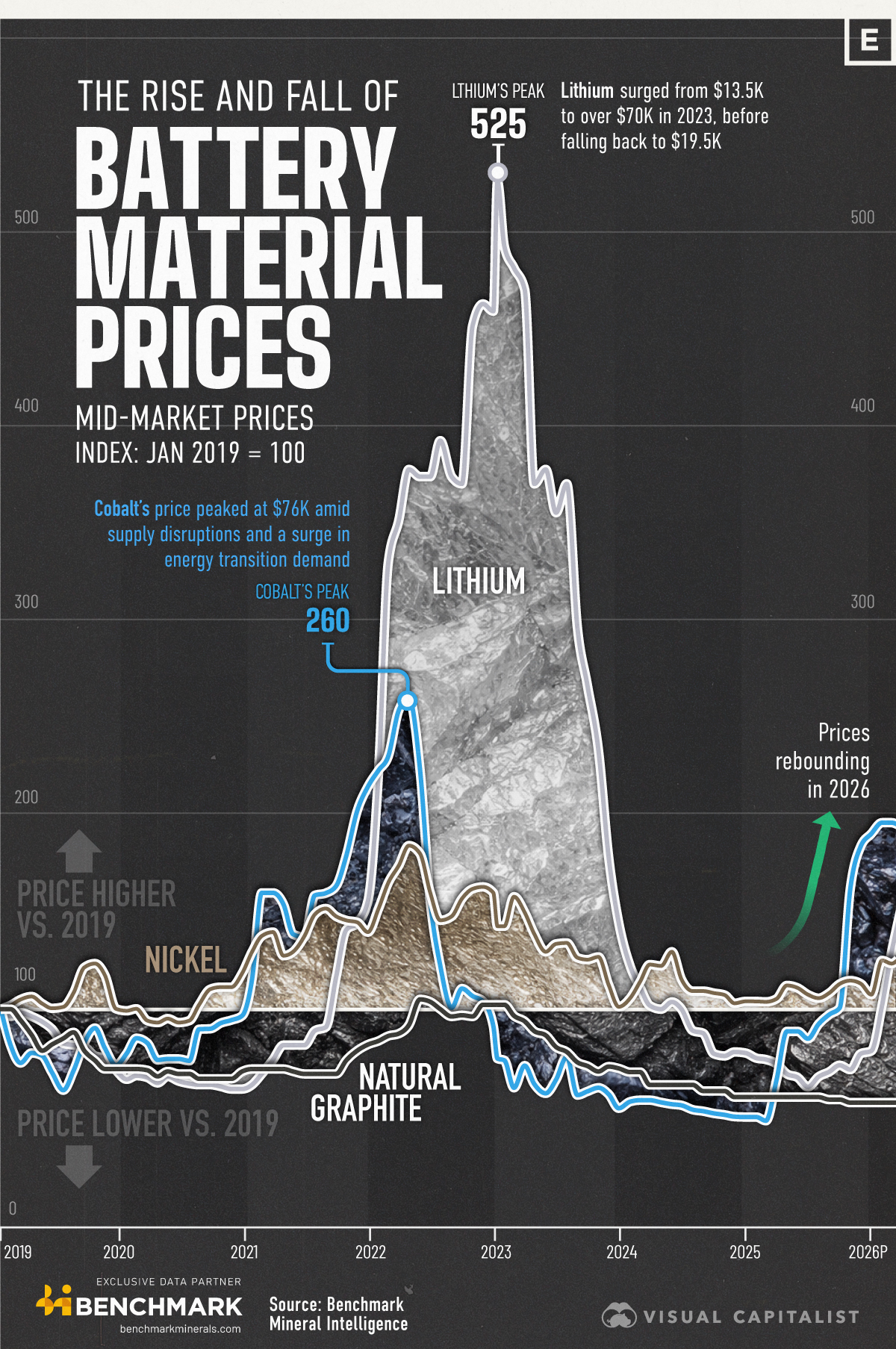

Beginning in 2021, battery raw materials saw huge price gains affecting lithium, nickel, cobalt and natural graphite. By 2024, these increases had been reversed – though prices are again on the rise.

Benchmark principal price analyst Adam Megginson explains that “battery raw material prices soared across the 2021–2023 period as demand for battery cells from the electric vehicle (EV) market met inelastic raw material supply”.

This, he adds, triggered “frenzied overbuying and an outsized supply response, combined with moderating EV sales growth”, in turn leading to “a slump in prices across the board, erasing all raw material gains in just 12 months”.

Demand dip as China EV purchases dropped

Benchmark’s lithium carbonate prices hit a peak of $81,375 per tonne in China by December 2022, before battery manufacturers responded by slowing production rates and delaying purchases. Combined with economic headwinds in China affecting EV purchases, this resulted in a price downturn before the turn of 2024.

Weak downstream demand for cobalt- and nickel-containing batteries led to falling prices for those minerals by 2023. Technological improvements facilitating the blending of part or most needle coke with lower-cost coke inputs also drove down the premium between high-energy synthetic graphite anode and the natural graphite alternative, though both dropped in price from 2022–24. Low-energy synthetic graphite demand growth was particularly pronounced as prices fell, with many OEMs switching to synthetic for energy storage applications when the cost of synthetic dropped below natural, as overcapacity in China allowed synthetic to maintain its competitive pricing.

Sulphur supply squeeze in 2026 increasing costs

In 2026, however, prices are rebounding, as some markets have seen major disruptions. Those include the war in the Middle East, which is squeezing supply of sulphuric acid, resulting in increased production costs across the battery supply chain. According to Benchmark analysis, as much as 59% of lithium supply is exposed to sulphur and sulphuric acid supply crunches, while a range of other battery materials are also likely to be affected.

Megginson also notes that energy storage has become “a new epicentre of demand growth”. In Q1 2026, installations of utility-scale storage in Europe doubled compared with the same period in 2025. In March 2026 alone, more was installed across the continent than in the entire year of 2023.

“Supply, however, is responding more slowly this time around compared with the 2021–23 period,” Megginson says. "The result is the current upward trend in prices.”

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.