Fluorspar: The quiet achiever of the lithium ion battery boom

While cobalt, nickel, and lithium hog the headlines, another critical mineral is quietly gaining prominence in the lithium ion battery revolution: fluorspar. Specifically, acidspar, a high-grade fluorspar concentrate, is emerging as a vital player in various stages of the battery value chain, driving demand and reshaping the industry’s landscape.

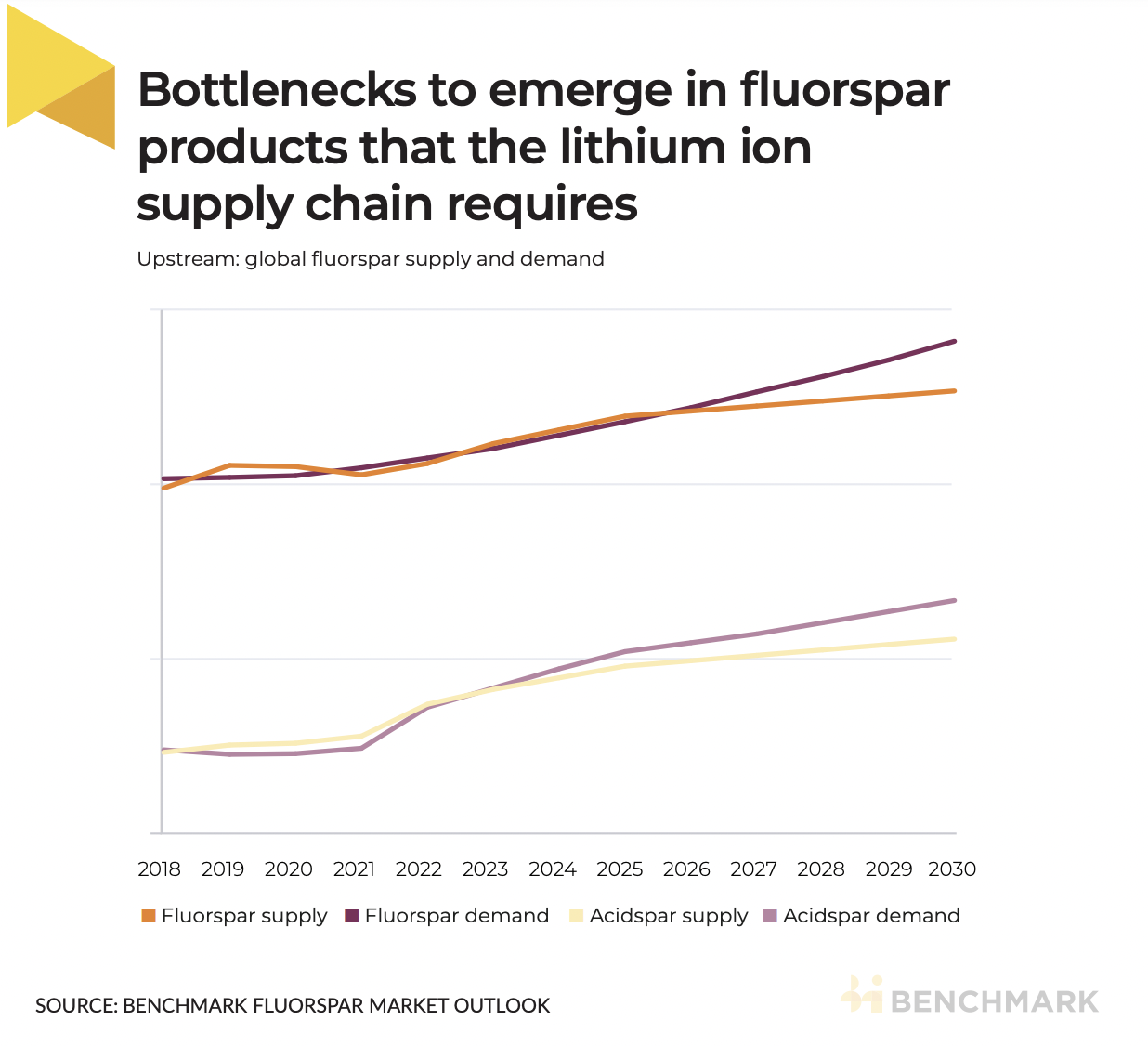

Fluorspar demand from the lithium ion battery sector is expected to exceed 1.6 million tonnes by 2030, representing a significant portion of the overall market, according to Benchmark’s Fluorspar Market Outlook.

This unassuming mineral, primarily composed of calcium fluoride (CaF2), holds potential beyond its traditional uses in refrigerants, steelmaking and aluminium production. Fluorspar is mainly produced through open pit operations and has two main grades: metallurgical-grade (metspar) for steelmaking and acid-grade (acidspar). The material is extracted and then processed through crushing, grinding, and physical sorting.

Acid-grade material or acidspar requires further chemical refining to reach 97% CaF2 content. The final product is sold in a powder form and transported either as dry or wet filtercake, depending on the shipping routes and end-market.

As the lithium ion battery market experiences exponential growth fuelled by electric vehicles and renewable energy storage, fluorspar’s unique properties are finding increasing application in four key areas:

1. Polyvinylidene fluoride (PVDF) binder in cathodes: PVDF, a fluoropolymer derived from fluorspar, serves as the critical binder material holding cathode active materials together. Its excellent performance in high-voltage batteries and resistance to harsh chemical environments make it irreplaceable. The growing demand for high-nickel cathodes, with their superior energy density, further boosts PVDF consumption.

2. PVDF coating on separators in pouch-format cells: Pouch cells, popular in consumer electronics and smaller battery applications, employ separators coated with PVDF to enhance their stability and safety. This application, though currently smaller than cathode binder use, is witnessing rapid growth due to the rising popularity of pouch cells.

3. Lithium hexafluorophosphate (LiPF6) electrolyte: LiPF6 serves as the key electrolyte salt in lithium ion batteries, facilitating lithium ion movement. Its production relies heavily on hydrofluoric acid (HF), which is derived from fluorspar. The surging demand for lithium ion batteries directly translates to increased LiPF6 and, consequently, fluorspar consumption.

4. Hydrofluoric acid for anode purification: Natural flake graphite, a common anode material, often contains impurities like silica. HF plays a crucial role in removing these impurities, enhancing the performance and safety of the anode. As demand for high-purity graphite increases, so does the reliance on HF and, subsequently, fluorspar.

Challenges ahead

This growing demand presents opportunities for the fluorspar industry. However, challenges remain.

Supply constraints: Current fluorspar production is largely concentrated in a few countries, raising concerns about potential supply bottlenecks. Additionally, stringent environmental regulations can hamper new mine development, further tightening supply. New, largescale, and high-grade mining projects can require large amounts of new capital which can present challenges in jurisdictions with high-risk profiles.

Price volatility: Fluorspar prices have historically been volatile, impacted by factors such as geopolitical tensions and fluctuations in demand from other sectors. This volatility can create uncertainty for battery manufacturers and hinder long-term planning. Diversifying supply and improving price transparency will help to remove some of the uncertainty from this critical market.

Sustainability concerns: Fluorspar mining and processing raise environmental concerns, necessitating responsible practices and the adoption of sustainable mining and processing technologies. Again, diversifying supply away from artisanal producers – particularly in China – is likely to improve the sustainability credentials of the industry. This is particularly true if additional supply can be funded in nations which already have an advanced and sophisticated mining industry.

Despite these challenges, the long-term outlook for fluorspar, particularly acidspar, is promising. The crucial role it plays in lithium ion battery production, coupled with growing demand for cleaner energy solutions, is driving innovation and investment in exploration, processing, and sustainable practices.

Looming deficits are encouraging supply through innovation but “grade is king” is still expected to remain the market mantra through to 2030:

Fluorspar is no longer a supporting actor in the lithium ion battery market. As the demand for cleaner energy solutions intensifies, acidspar’s critical role in battery production positions it to become a cornerstone of the sustainable future. Addressing supply chain challenges, reducing price volatility, and prioritising sustainability will be crucial to unlocking the full potential of this mineral in the burgeoning lithium ion battery revolution.

Benchmark has just launched its new Fluorspar Market Outlook with detailed analysis of supply, demand and prices out to 2030.

The report is updated every quarter to support market participants with their market activity and strategic planning.

If you would like to speak to Benchmark’s experts to learn more about our Fluorspar Market Outlook, please provide your details below and our team will be in touch.

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.