Infographic: Battery material production expansion since 2020 driven by shifting chemistry

:format(auto):focal(center))

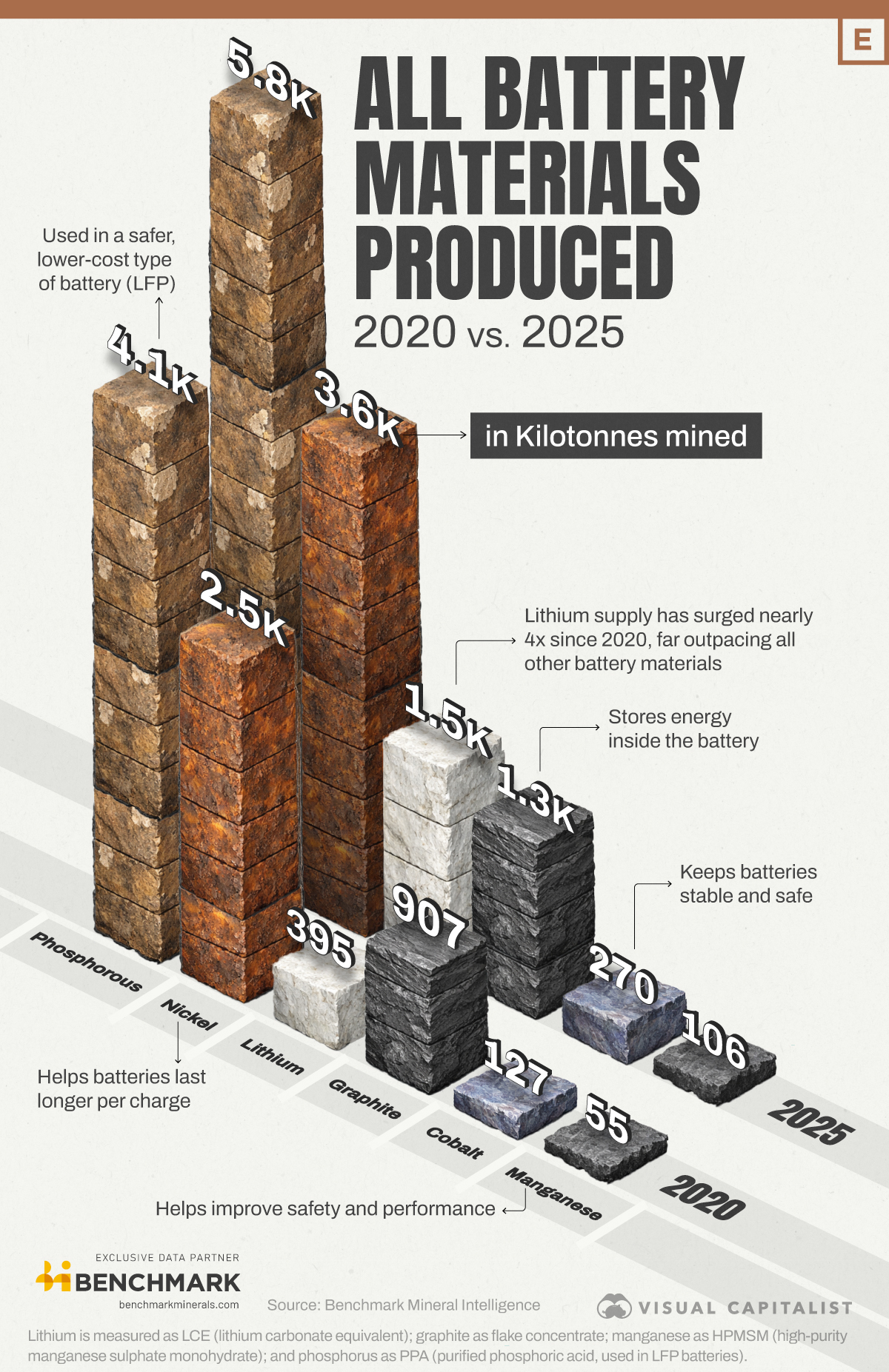

Production of battery materials has rocketed since 2020. Lithium in particular has surged, while other essential inputs like phosphorus and nickel have also grown as both lithium iron phosphate (LFP) and nickel cobalt manganese (NCM) battery production have ramped up.

In 2025, lithium production reached four times its 2020 level, growing from 395kt mined to 1,500kt. As lithium is used in almost all modern battery chemistries, its growth far outpaced other battery materials. Reflective of the growth of LFP chemistry, is the increase in the supply of purified phosphoric acid, which grew 41% from 2020–2025.

Nickel, the key input for NCM, grew from 2,500kt to 3,600kt across the same period, while cobalt and high purity manganese sulphate monohydrate also both more than doubled.

Nickel, the key input for NCM, grew from 2,500kt to 3,600kt across the same period, while cobalt and high purity manganese sulphate monohydrate also both more than doubled.

Battery chemistry shift driving material demand

In 2020, LFP’s global market share sat at 19%, compared with a combined 80% market share for nickel-based chemistries. By 2025, that had become a 60% share for LFP and a 44% share for nickel. China’s rapid expansion of battery production, combined with its focus on LFP, has underpinned this shift. By 2030, Benchmark forecasts LFP to extend its lead further to 71%.

Benchmark Intelligence is your gateway to more content like this, including articles, briefings, videos and over 2,500 prices across the mine-to-grid supply chain. To learn more, fill out the form below and one of the team will be in touch.

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.