Investment in battery gigafactories nears $300 billion since 2019 as China extends battery dominance

:format(auto):focal(center))

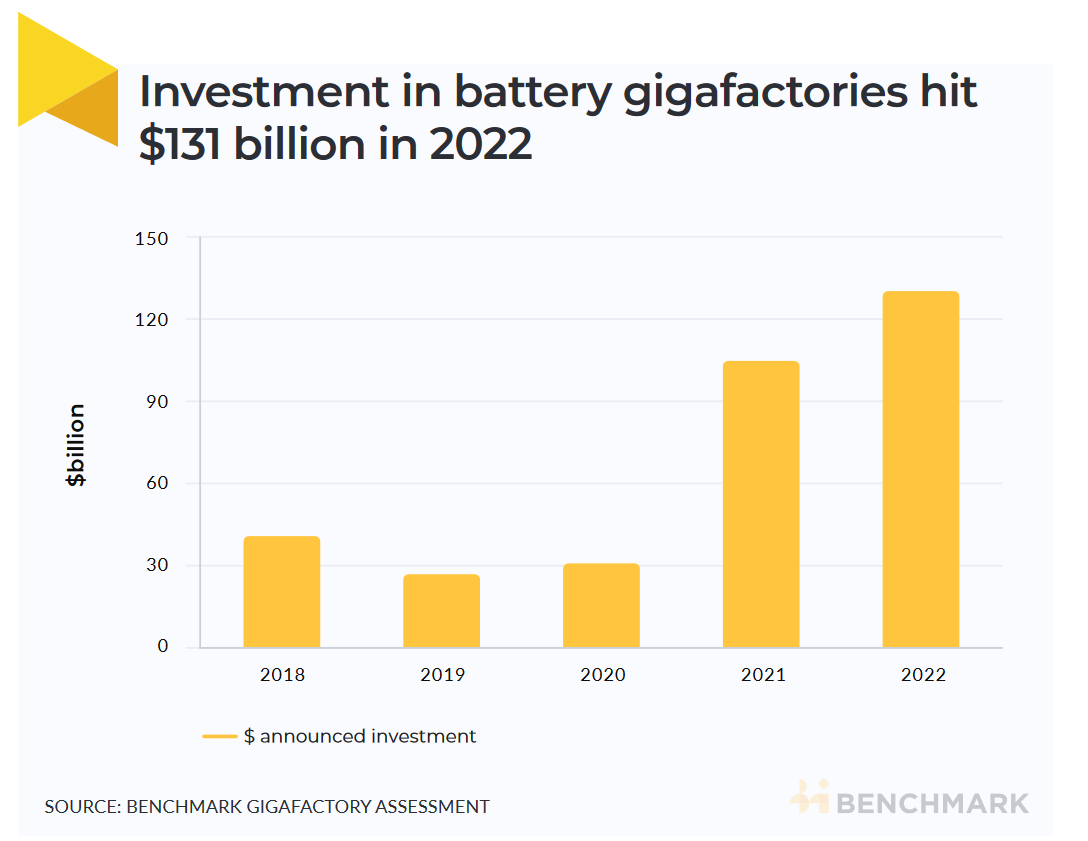

Almost $300 billion of investment in new lithium ion battery gigafactories has been announced over the last four years, driven by the rapid rise of the industry in China, which is home to the world’s largest producer.

A total of $131 billion of investment was committed last year, according to Benchmark’s Gigafactory Assessment, a 24% increase on the year before. China accounted for 74% of the total investment.

The global production of lithium ion batteries is set to increase five-fold by the end of the decade as a result of these investments, according to Benchmark. Last year the world added 102 gigafactories to the ten year pipeline with 3.1 terawatt-hours of potential new capacity.

China is set to remain the largest producer by the end of the decade due to the scale of its investment in new capacity. Benchmark forecasts China will produce 69% of the world’s lithium ion batteries in 2030.

The world’s largest battery producer, CATL, announced $12.6 billion of investments in new battery capacity last year, according to Benchmark. It is on track to have battery production capacity of 1042.6 GWh a year by 2031.

The company raised $6.7 billion in a private placement of shares in June. Its rival CALB raised about $1.3 billion by listing on the Hong Kong stock exchange in October.

“China still dominates the majority of the new investments,” Evan Hartley, an analyst at Benchmark, said. “Many of China’s top Tier One and Tier Two players raised significant financing during the year.”

US gets serious

Battery investment accelerated in the US last year, however, due to the passage of the Inflation Reduction Act in August, with $20.8 billion committed during the year.

As a result, North America is catching up in terms of the rate of new investments. China’s pipeline capacity grew by 65% year-over-year in 2022 to 5462 GWh, while North America’s increased by 49.0% to 1046.6 GWh.

Europe, meanwhile, increased its pipeline capacity 39.5% from 855.2 to 1,193.2 GWh.

Cost inflation

Still, the US will need to spend more for the same amount of additional battery capacity as China, especially in an environment of higher inflation and interest rates.

North American gigafactories are, on average, 46% more expensive to build per gigawatt-hour than Chinese gigafactories, at an average cost of over $100 million for a GWh.

LG Energy Solution’s planned $1.3 billion plant in Arizona, for example, would cost around $127 million for a GWh of production. LG said in the summer it was reviewing the plant due to rising construction costs.

China’s average is around $72 million for a GWh of new battery production capacity, although some plants are below $55 million per GWh.

The cost of expanding existing capacity, however, is considerably cheaper, especially on existing automotive production sites. Ultium Cells, the battery cell manufacturing JV of LG Energy Solution and General Motors, said it would invest only $275 million to expand the capacity of its Spring Hill plant from 35 GWh to 50 GWh.

The US government is also helping to finance construction of battery factories. Last month the Department of Energy announced it would provide a $2.5 billion loan to Ultium cells, GM’s joint venture with LG Energy Solution, for the construction of three battery factories.

BlueOval SK, a joint venture between SK On and Ford, has also applied for a government loan.

Tier One battery supply

Tier One battery suppliers currently dominate global investment in battery capacity, highlighting their ability to raise the necessary financing.

Benchmark includes CATL, Envision AESC, LG Energy Solution, Panasonic, Samsung SDI, SK On, BYD, Northvolt, Sunwoda as Tier One suppliers.

In the fourth quarter of 2022 a number of Tier 1 producers announced significant investments in China. Sunwoda said it would invest RMB 33.3 billion RMB ($4.7 billion) in two cell facilities in Hefei and Zhejiang, while CATL said it would invest RMB 14bn ($1.9bn) in a facility in Henan, with an expected nameplate capacity of 26 GWh.

Despite the scale of investment by Tier 1 suppliers, however, the demand for Tier 1 cells will outstrip supply over the next few years, with a growing deficit of cells expected from 2028, as EV and energy storage demand is expected to continue to rise as countries progress towards net zero targets.

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.