OPINION: What most major mining houses have got wrong about lithium

:format(auto):focal(center))

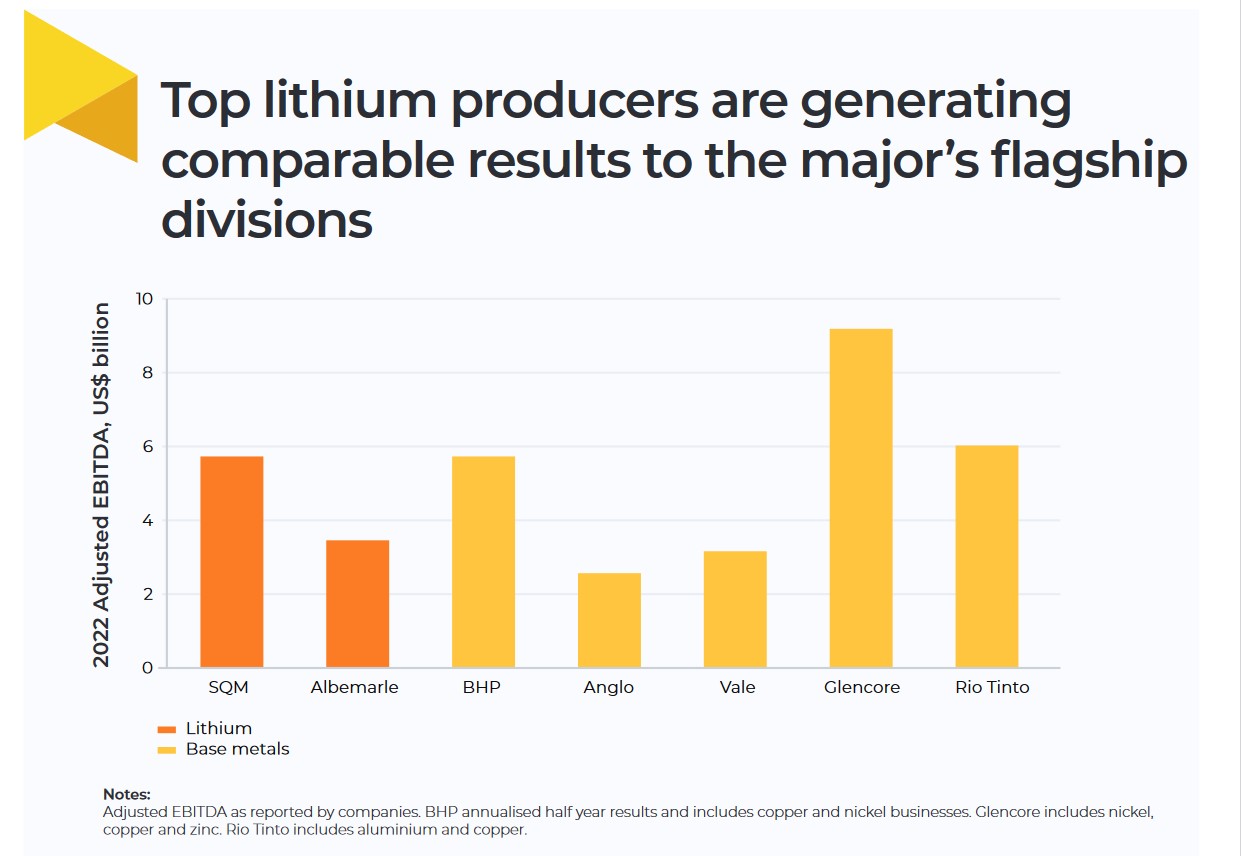

Major mining companies not active in the lithium space may be surprised to see the 2022 earnings figures reported by global lithium leaders SQM and Albemarle.

At $5.8 and $3.5 billion respectively in terms of earnings before interest, tax, depreciation and amortisation (EBITDA), the amounts dwarf the most optimistic forecasts for new growth commodities such as potash, which BHP and Anglo American have invested in.

To put these numbers in context, Anglo’s base metals division (several copper and nickel assets) reported an EBITDA of $2.6 billion in 2022 and BHP’s copper division annualised result published last month was $5.6 billion.

Lithium’s theoretical “unattractiveness”

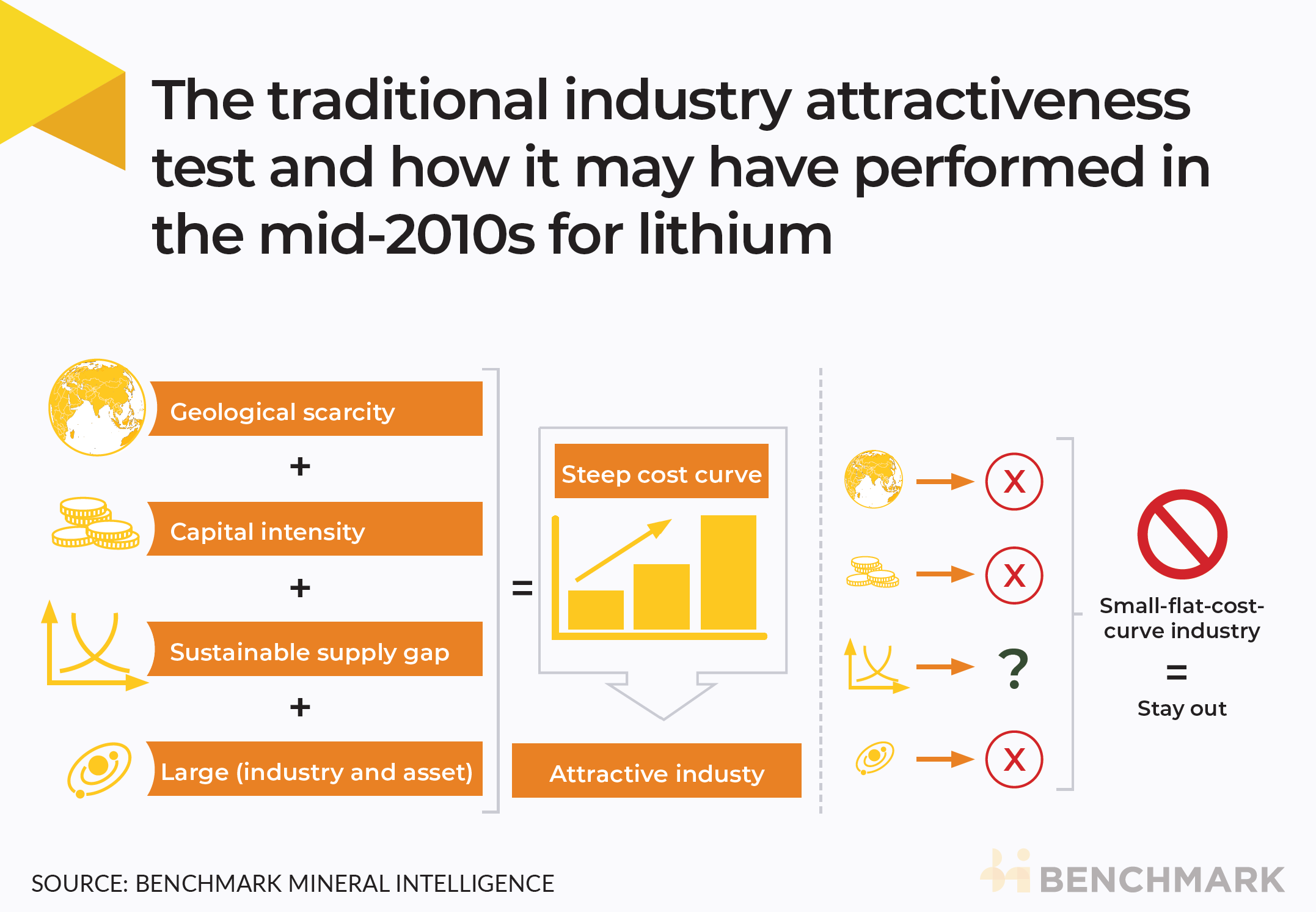

Traditional assessments of commodity “attractiveness” usually involve a view on a set of attributes that would drive a sustainable steep cost curve, such as geological scarcity, capital intensity, and supply gap profile, among others.

The hope is that, helped by superior financial capability, majors can establish themselves in the first two quartiles, leaving smaller high cost operators to set the price cycle (swing producers).

Some sophisticated analyses may include “resilience” during the low part of the price cycle – which essentially informs whether uneconomic supply is too sticky and therefore prone to prolong low price periods.

Don’t forget that the size of the industry must be large enough to deploy the heavy resources of major mining houses.

Lithium has not performed well under this test – in particular five years ago when the lithium fever started. It failed very early on by not being geologically scarce – according to the US Geological Survey lithium ranks as the 30th most abundant element on earth.

At 89 million tonnes, we have more than 130 years of 2021 production in known mineral resources (and resources have almost tripled from 2017). Many mining majors, driven by a “geoscience-first” approach, stopped right at that point.

There may have been others with enough patience to look further, but they again found disappointment in size and capital intensity measures. The total industry size of lithium in 2015 was a mere $1.6 billion and was forecast to reach no more than $8-10 billion by 2020.

“Why bother with a small-flat-cost-curve industry,” was the natural outcome of that traditional analysis.

The attractive reality of lithium

The conventional industry analysis for lithium appears to have aged badly (and too soon).

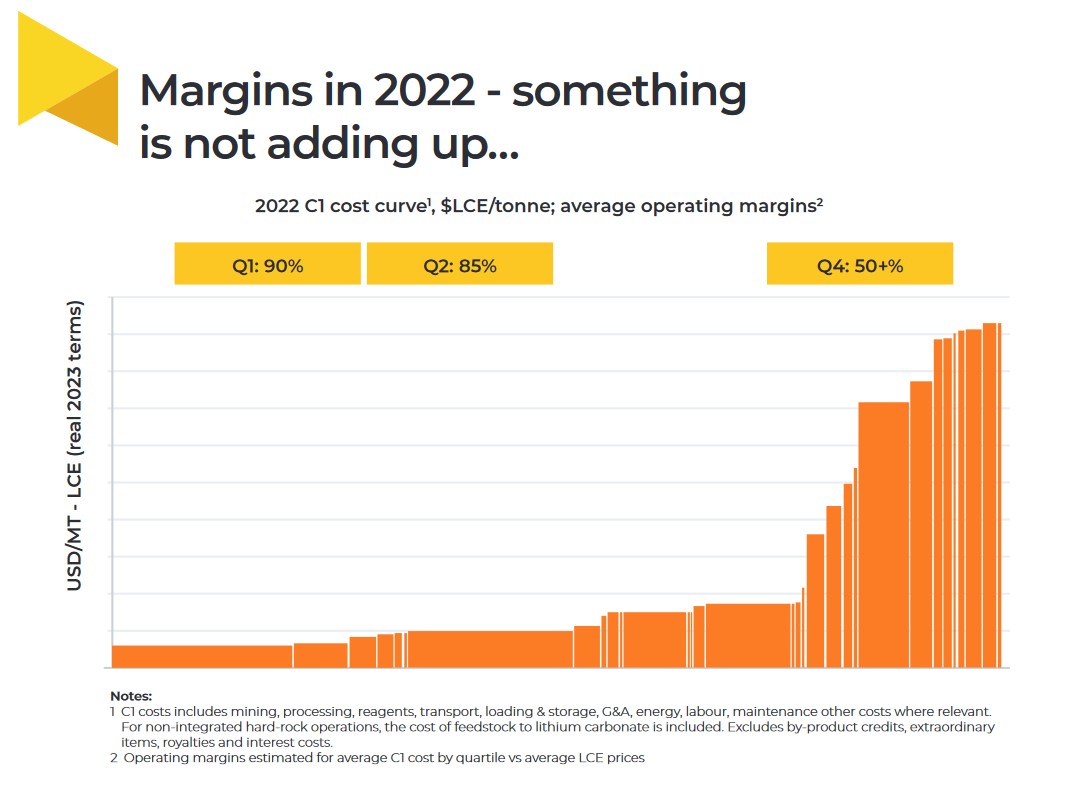

According to Benchmark’s leading price assessments, apart from 2020, lithium prices have been well above the marginal cost of production since 2017 and are forecast to stay at that level until early 2030s.

To put this in context, if copper had the same price levels in 2022 as the “adolescent industry” (as some commentators have referred to lithium), it would have traded at between $30,000 to $40,000 per tonne!

Furthermore, the industry is fully governed by a steep cost curve with first quartile and second quartile incumbents enjoying a juicy operating margin of 90% and 85% respectively last year.

And this trend is likely to continue. According to Benchmark’s industry leading lithium cost models, by the early 2030s the long run cost structure is likely to support operating margins above 50% for Q1 and Q2 operators.

Why the disparity between theory and reality?

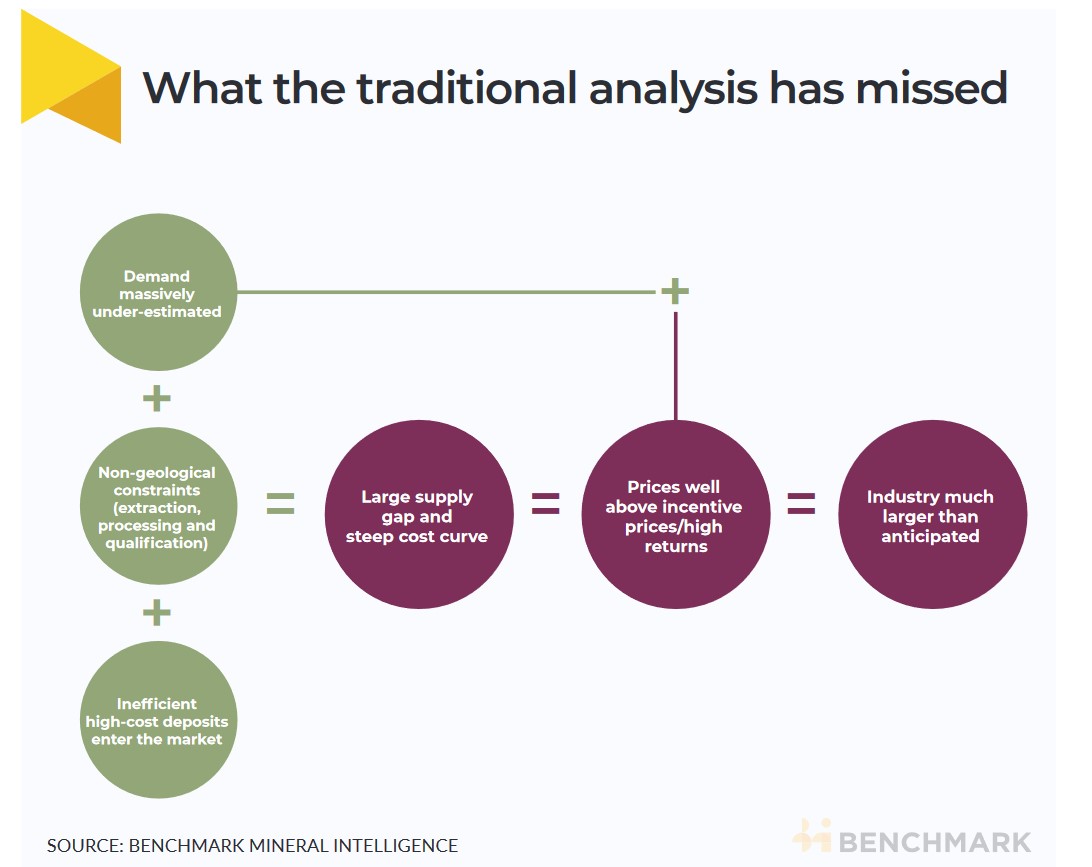

Our analysis indicates that there are two flaws in the traditional analysis.

The first missing link is on the constraints that exist to extract and process lithium to keep up pace with breathtaking demand. In other words, yes there may be “almost-unlimited” lithium units on the ground but what sets the price is the actual quantity of units that reach the market relative to (very high) demand. The natural question is then: why is supply so constrained?

There are two main bottlenecks: extraction and processing.

For extraction the issue is the usual lag in permitting and getting the resource mature enough to attract funding for construction – so in a way similar to other commodities, but again no other major commodity has a 15-year CAGR of 20%.

There are only so many geologists, engineers and permitting professionals that will be available to progress the extraction part of an “unattractive industry” at pace, even less when these capabilities are tightly held by the majors.

If you are lucky enough to get your extraction part sorted, that’s when the real problem starts. Lithium units going into batteries must be qualified along the supply chain – and this involves achieving specifications at the ppm (parts per million) level very early on.

As a result, the processing demands are enormous for “bulk chemists” ramping up new plants.

Qualification processes take 12 months, can fail and add an enormous commercial risk to mine development via compounded project risk. The same applies for anyone setting up merchant lithium chemical plants – feedstocks would need to be qualified.

It can become a classic “chicken-and-egg” situation.

The second gap in the traditional analysis is paradoxically on geology. A long period of time with prices well above incentive price levels has enabled a scramble to get to market as soon as possible.

That means it’s not the most efficient mineral resources that are being developed first. There are in fact plenty of previously thought uneconomic (now marginal) deposits that are entering the mainstream supply chain (lepidolite probably the most covered case). The result is therefore a cemented steeper cost curve than the traditional analysis would have suggested, leading to resilient and better than expected returns for low-cost incumbents.

The result of very high prices has led to an industry many times larger to what was forecast in 2015 – at $48 billion in 2022, which is still a long away from copper ($160 billion) or nickel ($80 billion), but nowhere near the $8-10 billion most conventional analyses were indicating in the mid 2010s.

What now for mining majors?

While hindsight could be painful for those majors that may have contemplated entering the industry in the mid-2010s, the reality is that attempting breaking in today would not be easy given the very high price environment which will expose them to write-downs in the future.

Majors should nevertheless refresh their views on the industry and explore areas in which they can play to their strengths (they do have large scale processing and project development capabilities).

The classic opportunistic/countercyclical M&A play should also be prepared if and when prices get back to, or below, incentive pricing (if only for a very short period of time though).

Finally, hindsight has a reputation as the only perfect science, but it is also a great source of learnt lessons. Geoscience is rightly at the centre of investment appraisal processes, but lithium has shown that while necessary, geoscience on its own is not sufficient to grasp the complexities of superfast growing commodity markets.

Benchmark’s Consultancy division advises mining companies and supply chain participants on market assessment and entry strategies, as well a wide range of business areas.

Please provide your details below to speak to our global team of experts on the opportunities and challenges facing your business.

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.