Spodumene prices soften to three year low amid weak lithium chemical prices

:format(auto):focal(center))

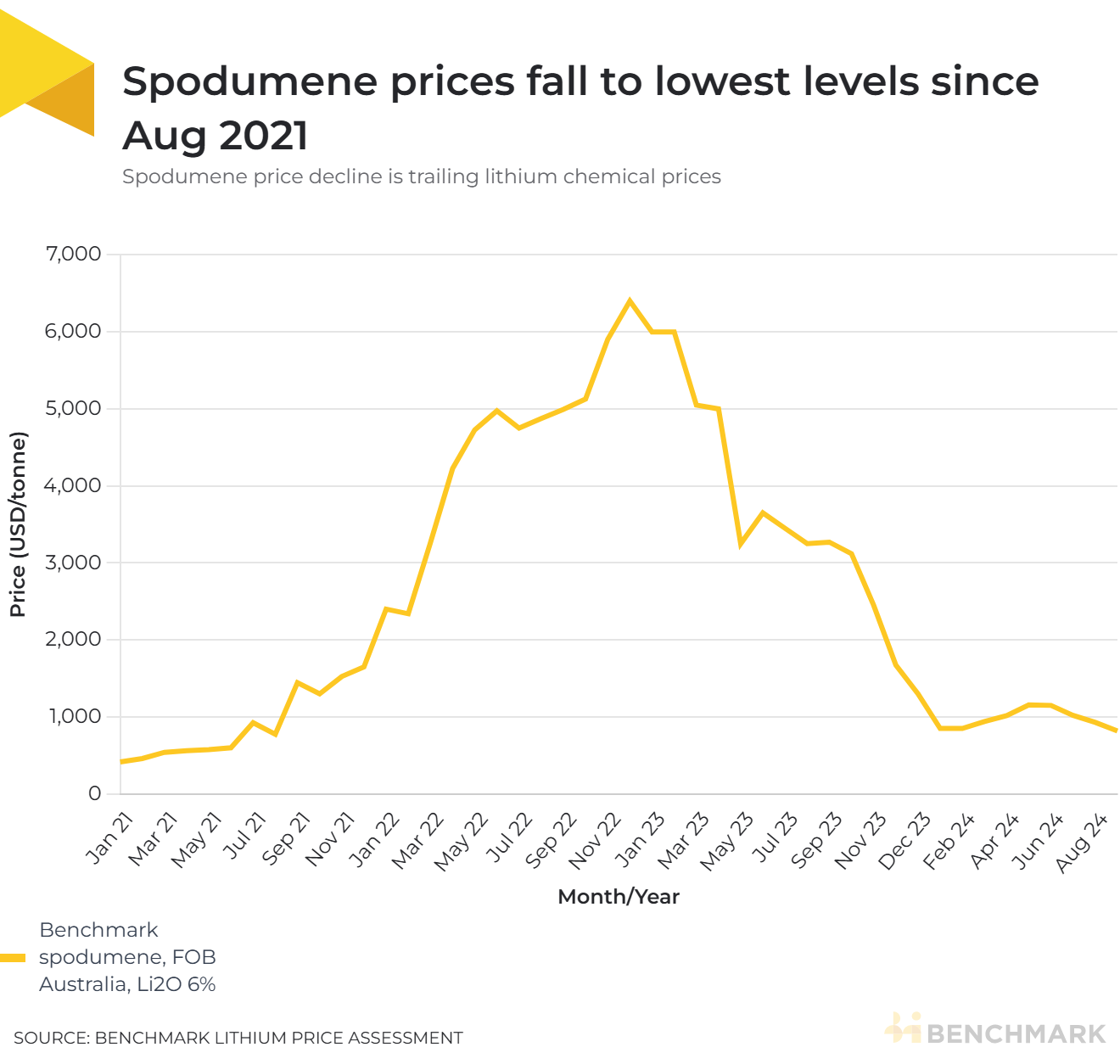

Spodumene prices fell to their lowest levels since August 2021 in early September, trailing the steep drop in prices of lithium chemicals in recent months.

Spodumene FOB Australia prices have fallen 14.4% so far this year to $818 per tonne in the assessment period ending September 4, according to the Benchmark Lithium Price Assessment. Prices have shrunk to one eighth of the peak levels of $6,401 per tonne seen in December 2022.

“The decline this year is very much driven by lithium chemical prices. Historically, spodumene prices follow the chemical price movement and there has been a continuous fall in chemical prices,” said Sophia Jang, analyst with Benchmark.

“Furthermore, there are significant inventories with suppliers and the spodumene producers in China continue to produce materials to maintain their market share,” said Jang.

Spodumene prices also notched a 3.3% decline in the two week assessment period ending September 4, exacerbated by a significant drop in lepidolite prices in China in August, making the latter an increasingly more attractive feedstock than spodumene.

Spot prices for lithium carbonate and lithium hydroxide in China have declined 23.8% and 15% so far this year for the period ending September 4, according to the Benchmark Lithium Price Assessment.

What do current levels mean for producers?

The declining prices have hurt the profitability of spodumene producers, especially for the higher cost producers, pushing them to cut production or delay project expansions.

“As we have approached the $800 a tonne mark, we have started to hear lower bids but they have not closed. So, we’re beginning to see resistance at these levels,” said Adam Megginson, senior analyst with Benchmark.

According to Megginson, producers don’t want to be the first to announce production pauses amid falling prices as it highlights that they are a higher cost producer. They also want to be ready and producing as prices climb back to be able to capture market share. As a result, some upstream players continue to produce despite prices falling below their costs.

This week Arcadium Lithium announced plans to put its Mt Cattlin mine into care and maintenance in 2025, citing the low price environment.

“I think we’re at a low point now, if you look at the publicly listed Australian miners, all of them are losing money now, except for Greenbushes,” said Cameron Perks, analyst with Benchmark.

“We still expect P1000 from Pilbara to come online, although it could be placed on ice if prices stay low. Greenbushes’ CGP3 expansion is coming online next year and potentially ramps up to around 60,000 tonnes a year lithium carbonate equivalent (LCE). This is still profitable, so it’s unlikely this will slow down. In Africa, projects are not slowing down, primarily owing to their Chinese ownership and vertical integration,” said Perks.

Are more declines coming?

Prices are, however, likely to remain bearish in the near term as besides falling lepidolite prices contributing to weaker demand for spodumene, producers are stocked with sufficient inventory.

“The price increase will not be significant until the end of this year. Though contacts have expressed there could be a short-term increase in price in late September as Chinese cathode producers procure material in advance of the National Day Golden Week on 1 October. We expect demand to increase in the fourth quarter as historically the EV demand is highest then, but whether that translates to higher prices is another question,” said Jang.

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.