The top energy storage cell suppliers and system integrators in 2025

:format(auto):focal(center))

In 2025, over 600GWh of cells were shipped globally for battery energy stationary storage (BESS) applications, almost double that of 2024 as assessed by Benchmark's Battery Energy Stationary Storage Service.

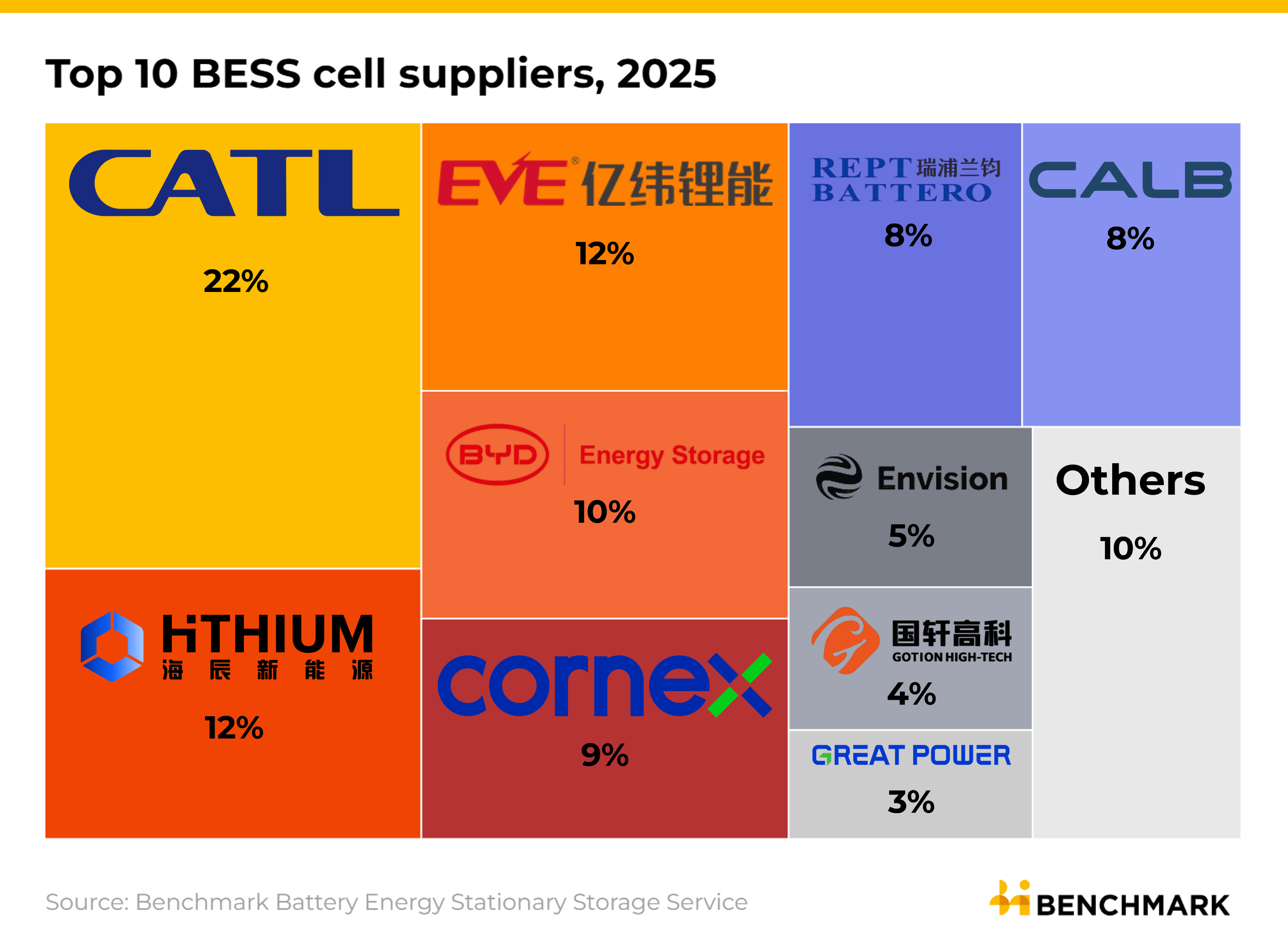

Combined, the top 10 BESS cell suppliers in 2025 accounted for 90% of cells shipped and all are headquartered in China.

“Notably the Korean cell manufacturers are missing from the top 10,” said Iola Hughes, Benchmark’s Head of Research. “That is likely to change in the coming years with significant commitments now made to BESS, in particular in the US market.”

In its Q1 financial report, LGES stated it is targeting over 50GWh of production capacity by the end of 2026. If it were to produce at this level, LGES would likely climb to within the top 10.

CATL continued to be the top supplier of BESS cells in 2025, representing 20% of the market. However, this is down from the 29% share the company held in 2024 and 32% share in 2023. Towards the end of 2025, it secured a three-year 200GWh deal to provide cells to system integrator HyperStrong. This deal was expanded to include 60GWh of CATL’s sodium ion BESS cells in April 2026.

CATL continued to be the top supplier of BESS cells in 2025, representing 20% of the market. However, this is down from the 29% share the company held in 2024 and 32% share in 2023. Towards the end of 2025, it secured a three-year 200GWh deal to provide cells to system integrator HyperStrong. This deal was expanded to include 60GWh of CATL’s sodium ion BESS cells in April 2026.

HiTHIUM and EVE Energy are both gaining ground on CATL. The two companies took second and third spots, respectively, with around 12% of the market each.

For HiTHIUM, this is a substantial jump from fourth position in 2024 when it represented 9% of BESS cells shipped. The company signed a five-year, 120GWh cooperation agreement in December 2025 with system integrator CRRC.

Although EVE Energy dropped down to third from second in 2024, it is still strongly competitive. In 2025 the company secured more than 10 cell offtakes of at least 1GWh including 50GWh with HyperStrong and 20GWh with Rochenergy. EVE Energy has also had a strong start to 2026, with over 40GWh of offtakes signed in the first quarter.

Another rapidly rising competitor is CORNEX, which has over 400GWh of production capacity under construction with a further 100GWh in the pipeline, though this is for both EV and BESS applications.

Who were the top BESS system integrators in 2025?

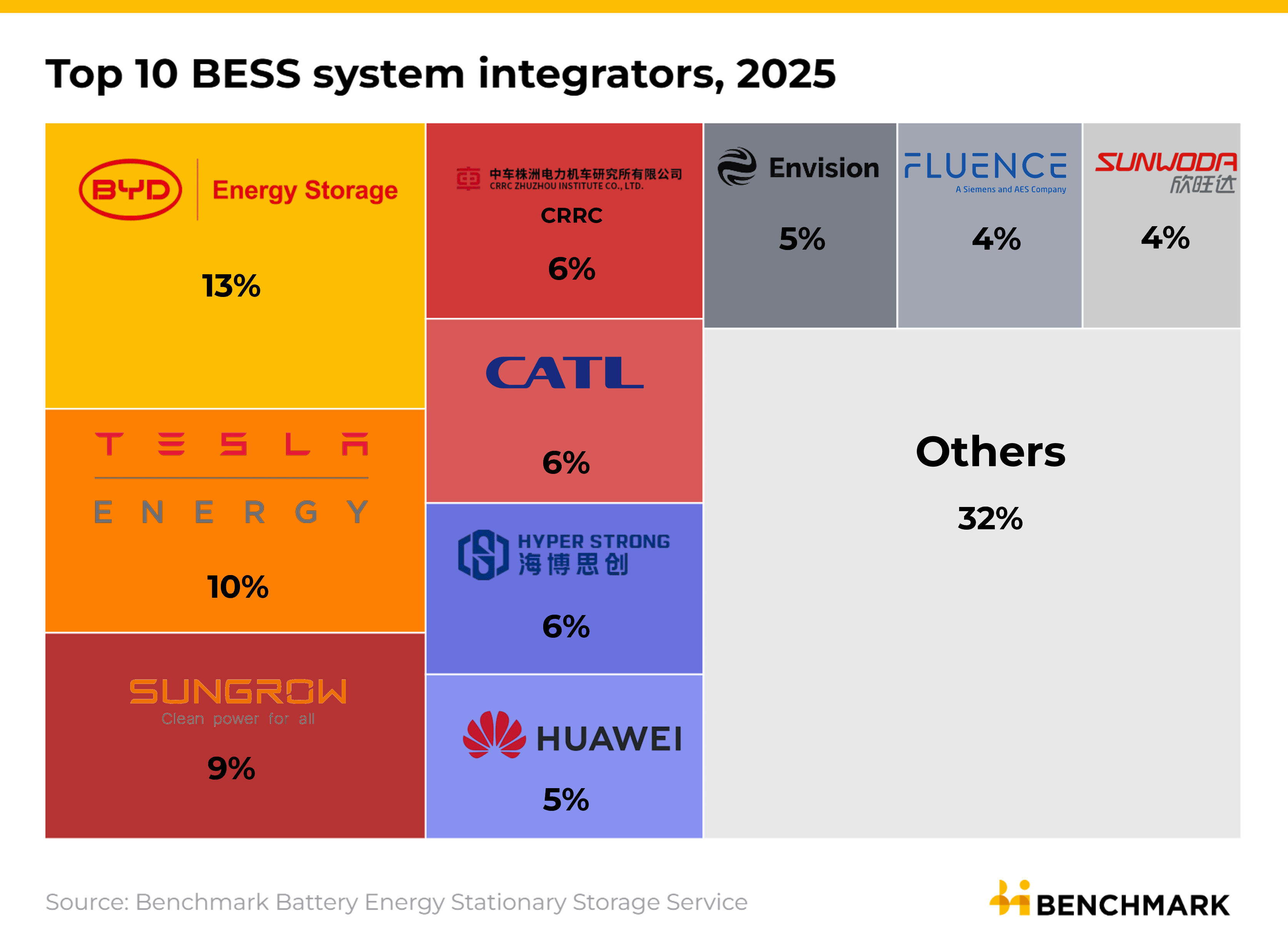

In 2025, around 460GWh of BESS systems were shipped globally with the market highly dominated by Chinese system integrators. Tesla and Fluence, both based in the US, are the only system integrators in the top 10 which are headquartered outside of China.

BYD overtook Tesla in 2025 to take the top spot for BESS systems, with Tesla now in second place and Sungrow in third. The three companies combined represented around a third of the systems market in 2025.

At the start of 2025, BYD signed to deliver a 12.5GWh BESS project with the Saudi Electricity Company, adding to the 2.6GWh already delivered.

Tesla’s BESS deployments for the full year 2025 reached 46.7GWh, growing 49% year-on-year, according to its annual report. The company says it will begin production of Megapack 3 at its Houston Megafactory in 2026, ramping up to 50GWh of manufacturing capacity. That said, Tesla has had a weaker start to 2026, with Q1 2026 BESS system installations down 15% year-on-year.

Tesla’s BESS deployments for the full year 2025 reached 46.7GWh, growing 49% year-on-year, according to its annual report. The company says it will begin production of Megapack 3 at its Houston Megafactory in 2026, ramping up to 50GWh of manufacturing capacity. That said, Tesla has had a weaker start to 2026, with Q1 2026 BESS system installations down 15% year-on-year.

BESS systems were the largest revenue segment for Sungrow in 2025, reaching 42% of total revenue surpassing its photovoltaic inverter business which accounted for 36%.

Many smaller Tier 2 and Tier 3 players reduced their net revenues in order to compete for market share leading to a price war and involution. As such, the share of companies outside the top 10 grew to 32% in 2025 compared to 18% in 2024.

The insights in this article were drawn from Benchmark’s Battery Energy Stationary Storage Service. To learn more about this, please fill in the form below and one of the team will be in touch:

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.