OPINION: Why battery supply chain investors should not fear disruptive technologies

:format(auto):focal(center))

Supply-side players, including upstream producers, refiners and battery manufacturers, seem to have recurrent nightmares about a new technology that will suddenly come and eat their lunch.

“Technology leapfrogging” is a central question we get asked when undertaking due diligence assignments or bankable market reports.

The concerns may be fed by a wave of investment from technology-savvy venture capital money, which has in the past enabled sudden cannibalisation of a product (e.g. digital cameras, media players, and sat navs made redundant by smartphones).

One area of concern for nickel and cobalt producers aiming to ramp up upstream production is the emergence of a new generation of lithium iron phosphate (LFP) battery technologies that are set to compete in the mid-range electric vehicle (EV) market where nickel cobalt manganese (NCM) chemistry incumbency is strong. Adding manganese to the cathode (to create LMFP) appears to do this by adding energy capacity at a marginal additional cost.

To add further pessimism, manganese is also being added to NCM cathodes themselves to significantly reduce nickel content and eliminate cobalt (NMx technology) with a potentially modest trade-off between cost and performance. Benchmark base-case forecasts suggest that both LMFP and NMx (also known as manganese-rich chemistries) are only likely to reach commercialisation at scale by the end of this decade and stay in single digits market share by 2040.

While lithium is almost immune to the manganese-rich chemistry battle above, upstream incumbents worry about the emergence of direct lithium extraction (DLE) as the equivalent to shale in the oil and gas industry a couple of decades ago. As discussed recently in a paper, we believe DLE does have a role in the sector, but development pathways are still uncertain and full-scale disruption is a low-probability event.

On the anode side, the concern is about solid-state batteries massively substituting incumbent graphite feedstocks. Again we have discussed the high degree of uncertainty of these technologies becoming mainstream by the end of this decade.

Incumbent battery makers have their own anxieties with sodium ion batteries making a massive leap to enhance their energy storage system appeal and compete head-to-head with lithium ion in the EV market. Benchmark’s view is that there are very significant technical challenges for that to happen.

Seen from these perspectives, it appears to be a matter of “when” rather than “if” incumbents lose out to disruptors. But does incumbency actually matter?

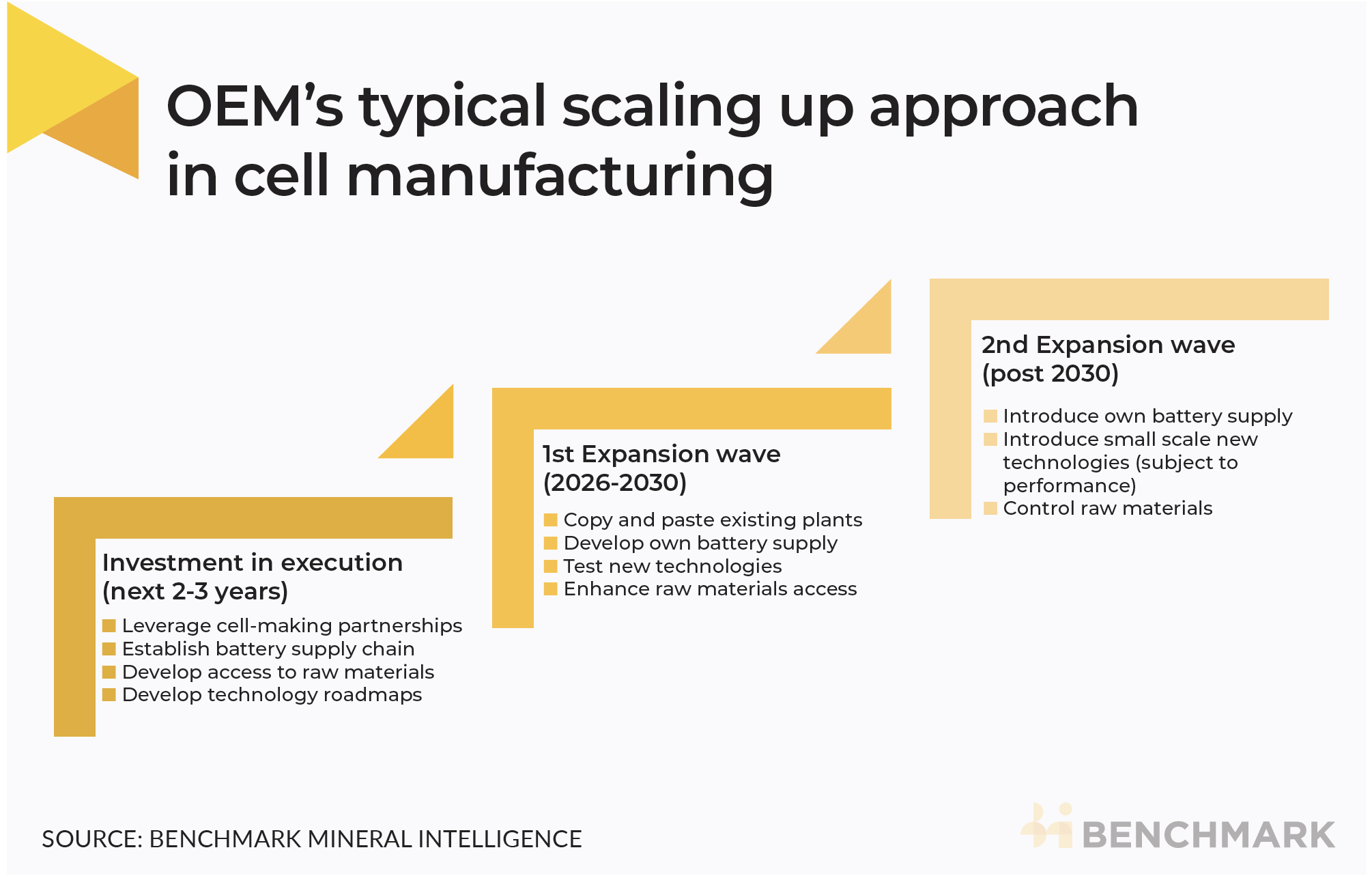

The role of incumbency and scaling up

One potential issue is that disruptive technology discussions are often made under a “point in time” perspective, missing the highly dynamic nature of the market.

A reminder: under Benchmark’s base-case outlook the lithium ion value chain needs to add in the next seven years three times as much as it has done in the last seven years. As a consequence, the overarching priority for OEMs is to scale up production as fast as possible, and new technologies, no matter how “plug-and-play” they are, will put this scaling up drive at risk.

New technologies, by their nature, create uncertainty and ultimately weigh on funding decisions by OEMs and cell makers.

This is not to say that incumbents are completely ignoring new technologies.

As shown above, serious incumbents are indeed considering new technologies, not for the expansions being sanctioned over the next three to five years, but for those further down the line in the next decade.

Such adoption, which is later than tech-developers are hoping for, is heavily caveated by technical performance requirements, to ensure beyond doubt that the new technology will deliver the promised benefits.

Incumbents have the capability to test new technologies in parallel to scaling up conventional plants, enabling optionality to introduce them at the right time. New entrants on the other hand cannot afford to double down on technical risk as it will undermine their entry efforts.

In short, the trade-off between faster scaling of production versus the potential benefits of new technologies does not work in the short term. The caveat to this is that if EV adoption slows down (there are plenty of economic headwinds), the urgency of scaling up is no longer there and a new technology may have a better chance of winning the trade-off.

But as has been experienced many times in the past, technologies tend to make slow progress over a long period of time to then suddenly leapfrog almost overnight to become mainstream. How would the lithium ion landscape change if the optimists are right?

Faster technology adoption

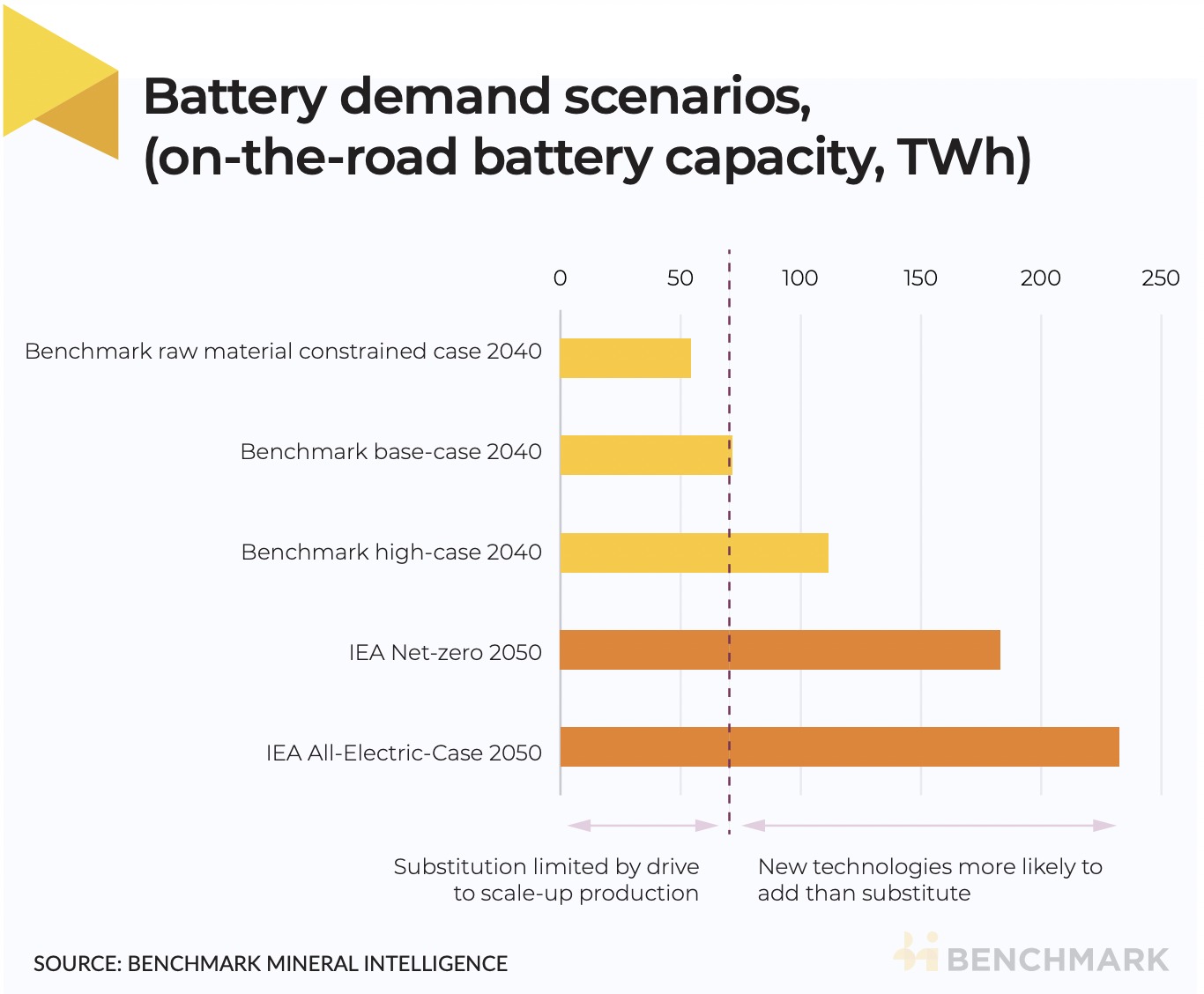

As a thought exercise let’s assume all of the above “base-case” views fail to materialise and every single technology becomes mainstream within this decade. The most salient outcome of this scenario would be a materially lower unit cost per kilowatt-hour and therefore an increased risk of new technologies substituting incumbents.

However, demand is likely to respond positively to lower battery costs. How strongly? The higher end of demand for batteries is what is needed to achieve Net Zero plans, which as shown below is materially higher than “base-case demand.”

The reality is that the world is massively constrained by a lack of raw materials, in particular lithium, to meet Benchmark’s base-case demand scenario, let alone to get to the International Energy Agency’s Net Zero or all-electric case scenarios.

Assuming the world manages to somehow debottleneck the upstream part of the value chain (not a light assumption to make), the upshot is that if these technologies do surprise us on the upside, then there is a case to be made that they will most likely add to rather than substitute supply. The end result will be a solid pathway to achieve net zero by 2050.

In practice though, it is likely that the bottleneck (and subsequent investor anxiety) moves to the associated infrastructure required for such massive and faster level of electrification – in particular availability of copper, grid expansions and charging infrastructure.

Benchmark’s Strategic Advisory team provides bespoke analysis and consulting services to enable the most complex investment decisions in the lithium ion industry, including how the interplay of different technology pathways could impact investors, policy and markets.

To learn moreplease provide your details below and our experts will be in touch:

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.