Rise of DLE will open up new sources of lithium supply this decade

:format(auto):focal(center))

The rise of Direct Lithium Extraction (DLE) technology promises to open up new sources of lithium supply this decade, helping to avert a forecast shortfall of supply, according to a new Benchmark special report.

DLE is an umbrella term for a group of technologies that selectively extracts lithium from brines.

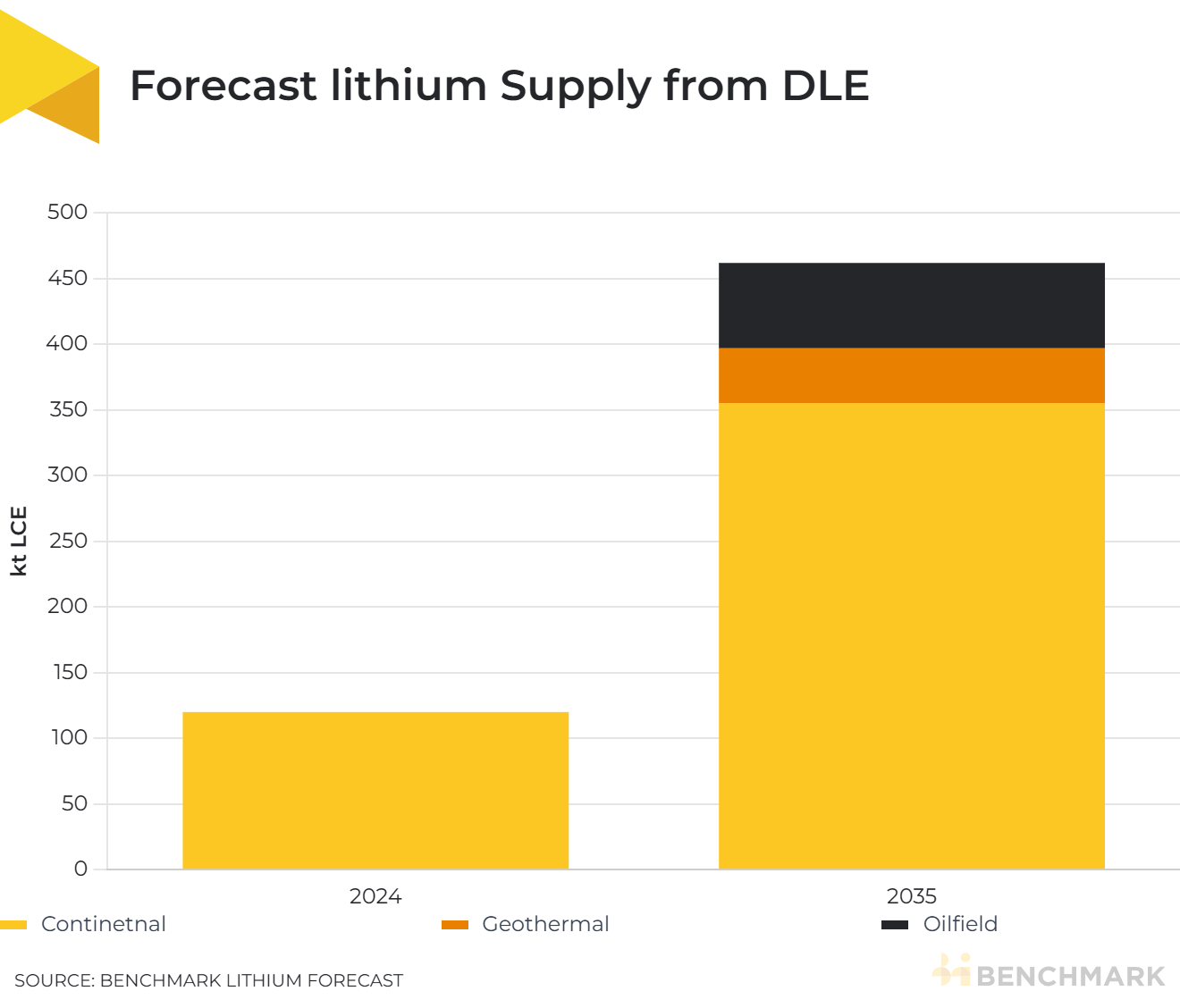

There are currently 13 operating DLE projects forecast to produce around 124,000 tonnes LCE of lithium chemicals in 2024. By 2035, DLE is expected to contribute 14% of total lithium supply, at around 470kt LCE, according to Benchmark’s Lithium Forecast.

The majority of the 2035 supply is set to come from continental brines, but with geothermal and oil fields expected to take a 9%, 14% share respectively, according to Benchmark.

Almost three-fourths of new brine projects will use some form of DLE, according to Benchmark.

The rise of DLE highlights a reality for supply over the next decade: the growing importance of unconventional supply and the expanding ecosystem of new players in the lithium value chain – particularly oil companies – who will bring capital and expertise to the industry.

However, DLE’s path to commercialisation could also take time, due to challenges around scalability, inflationary pressures, and delays at new brine projects. Technical risk also provides a hurdle for new investors in the sector.

Benchmark’s DLE special report provides an overview of the different DLE technology types including adsorption, ion exchange, solvent extraction, and membranes.

Adsorption is the most widely adopted and best-established technology, having been commercially applied by Arcadium and various companies in China.

Due to the uniqueness of each brine in terms of impurity levels and lithium concentration, there is no ‘one-size-fits-all solution’. Therefore, for each project, the DLE solution will likely need to be modified to meet the specific environmental and economic conditions.

Oil-field brines

The utilisation of DLE will open up previously undeveloped sources, namely those with low concentrations of lithium such as petro brines, and geothermal deposits. DLE has the potential for 80-90% recovery rates compared with the current evaporation yields of 20-50%.

DLE could also unlock vast “unconventional” brine resources located in western jurisdictions, at a time when building localised and diversified streams of critical minerals is increasingly a political priority in the US and European Union.

These “unconventional” resources include previously untapped geothermal and oilfield lithium-bearing brine resources, currently considered uneconomic due to lower lithium concentrations and an inability to extract lithium via traditional evaporation methods.

For this reason, DLE’s potential is attracting major players to the table. Amongst whom oil and gas companies are increasingly allocating capital and resources to the technology’s development, due to DLE’s similarities with upstream oil extraction and refining.

Standard Lithium’s Stage 1A project in Arkansas is forecast to be the first petrobrine project to come online in 2026 bringing an initial 5,000 tonnes a year to the market.

Oil giant Exxon Mobil is also investing in the state. Last month Exxon Mobil said it had signed a non-binding memorandum of understanding (MOU) with battery producer SK On for supply of up to 100,000 tonnes from the company’s DLE lithium project in Arkansas.

Cost challenges

Still, capital and operating cost challenges associated with lithium DLE projects have been less understood and appreciated by the broader market.

DLE projects have seen significant cost increases as projects advance, and feasibility studies are updated. Increasing capital cost estimates are attributed to rising global inflation rates, elevated equipment, utility and labour costs. For example, the average early-stage DLE project has an average capital intensity estimate of $37/kg LCE, while advanced projects average $60/kg LCE.

DLE is unlikely to be the silver bullet for the lithium industry in the short-term therefore and Benchmark doesn’t believe the technology alone is sufficient to bridge structural deficits in the lithium market.

Benchmark’s recent special issue – Direct Lithium Extraction: The rise and potential of new lithium extraction technology – explores this topic in further detail. Request your copy now.

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.