UK strategy needs to align with battery ambitions

:format(auto):focal(center))

The UK needs three to four supersized gigafactories to meet the 200 gigawatt-hours of batteries needed per year by 2030, according to Simon Moores, Benchmark’s chief executive

With the loss of Britishvolt earlier this year, the UK’s battery 2030 downstream pipeline is just 13% of this, with all of the UK’s forecast gigafactory production coming from Envision AESC.

In light of the US creating the Inflation Reduction Act to increase its domestic competitiveness and Europe’s Green Deal Industrial Plan, it is vital that the UK develops a cohesive plan to incentivise and encourage the development of its own battery ecosystem.

“An industrial strategy to attract the £20bn investment it will take to build at least three supersized battery plants isn’t there,” Moores said. “Joined-up thinking is then needed to attract the £60-80bn of investment to build the critical mineral supply chains that feed these gigafactories and recycle as much of the raw material at the end of life.”

Building British batteries

The UK’s only operating gigafactory is run by Envision AESC in Sunderland. With a capacity of 1.9 GWh, the facility produces pouch cells, primarily for Nissan.

In partnership with Nissan, Envision AESC plans to build a second UK gigafactory in Sunderland with an additional 35 GWh.

“There is a kind of a race in Europe to deliver these gigafactories,” Stephen Gifford, chief economist at the Faraday Institution, told Benchmark Source. “And while there’s probably space over the next two or three years to help develop and attract gigafactories, if we take much longer than that then we could lose the opportunities.”

Britishvolt, before it collapsed, intended to construct a 38 GWh gigafactory in England’s North East. But missed milestones, a lack of customers, and uncertain supply chains led to its failure.

“The Britishvolt model was always a challenging model,” Gifford said. “They had never built batteries before. They didn’t have a proven chemistry. And they didn’t have defined customers.”

The fall of Britishvolt shouldn’t be perceived as an indication of weak desire for batteries, Gifford said, but should serve as lesson for future battery aspirants in the country.

“You certainly will need for any manufacturing companies locating and building gigafactories in the UK, for them to really invest in building customers,” Gifford said.

One such development which may be taking on these learnings is the West Midlands Gigafactory, a joint venture between Coventry Airport and the Coventry City Council. The is currently takes the form of an attractive site in an industrially active region of the UK with access to a renewable electricity grid, but as yet no one to develop the site.

“You’ve got to have an investor, you’ve got to have all the supply side of it correct. But you’ve also got to have the customers,” Andy Street, the mayor of the West Midlands, said in an interview with Roger Atkins, founder of Electric Vehicles Outlook.

The West Midlands this week gained one potential customer. Jaguar Land Rover, owned by India’s Tata, announced Solihull as the location it would make its new electric “grand tourer” with delivery from 2025. The car is priced at £100,000.

Aligning industrial strategy

Historically, the UK’s primary strategy for developing a battery industry has been to focus on research and development, according to Gifford.

The strategy can be broken down into three components: The Faraday Institution focuses on basic, scientific research; Innovate UK focuses on collaborations between public and private; and the UK Battery Industrialisation Centre is focused on scaling up technologies.

The latter has a base in the West Midlands and is part of the West Midlands gigafactory’s attraction.

“This is perhaps the really, really important ingredient of our location in terms of being so close to so much of the R&D that’s going on in this sector, because that’s what will really drive investment in time,” Street said.

Beyond research and development is the Automotive Transformation Fund, which brings together governmental departments to incentivise companies to build gigafactories in the UK.

Joining up supply chains

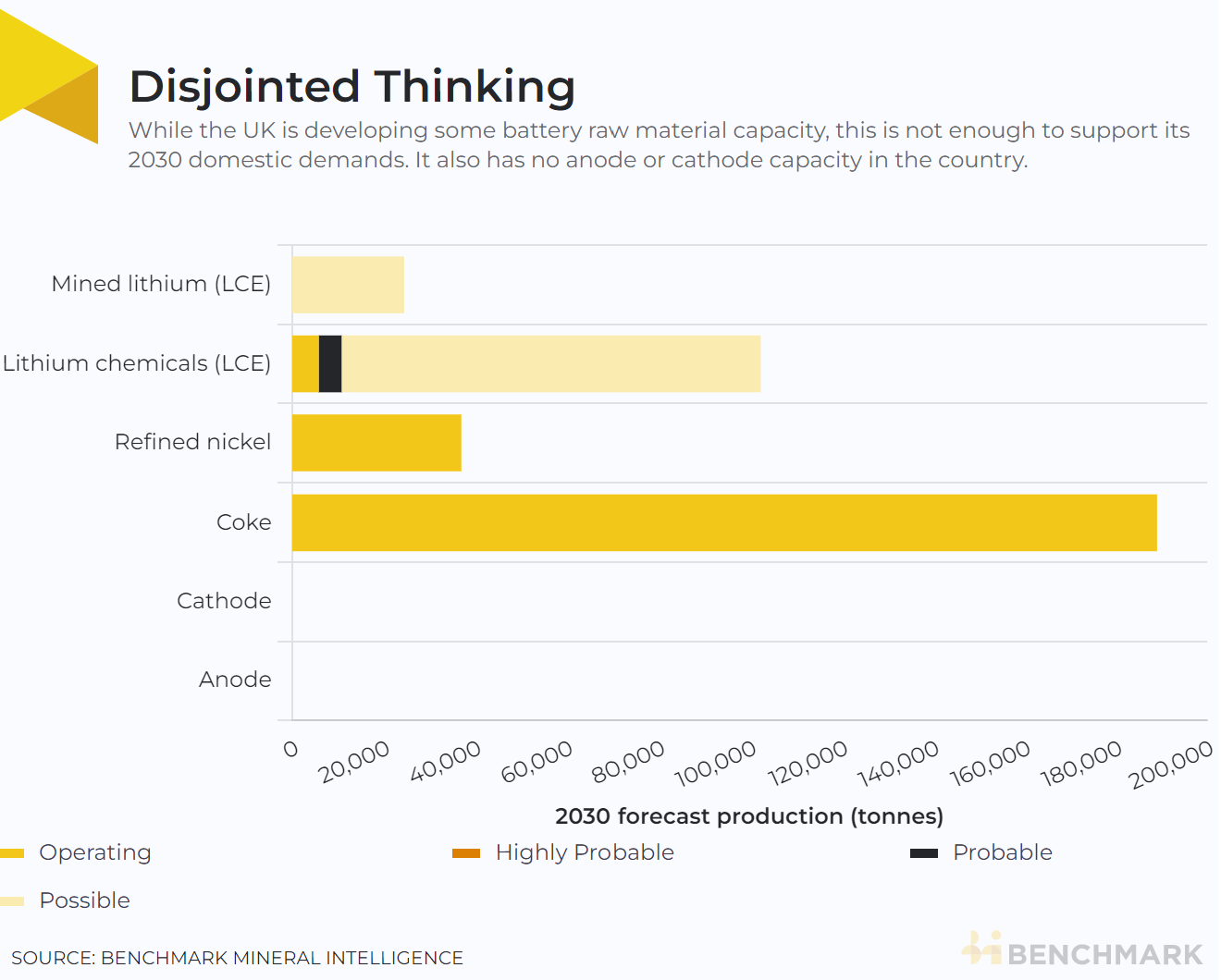

If the UK succeeds in building gigafactories to supply 200 GWh of domestic demand, it will need to invest in developing a supply chain to support these factories. Almost 160,000 tonnes of lithium will be needed, according to Benchmark.

Although the UK has some critical raw material developments, such as Cornish Lithium which is looking to mine lithium, the country is unlikely to produce much of the required minerals itself. It developed a Critical Mineral Strategy last year that aims to ensure the country has access to the materials needed for developing and future industries.

“From both the competitive cost side as well as the geopolitical angle, it is important to bring as much supply chain into the UK as possible,” Gifford said. “If they can mine it commercially in Cornwall, that’s going to be a good thing to diversify the supply chain. But really it’s not going to be the main source, or the majority of the source, for raw materials for a gigafactory in the UK.”

Recycling has the potential to make up a large part of the long-term material supply for gigafactories. However, end-of-life feedstock won’t be available in large quantities until at least the mid-2030s and the UK doesn’t have any substantial gigafactory capacity at present to provide the process scrap that could feed recyclers in the interim.

“[The UK] does have a [recycling] strategy, and it does have a vision,” Gifford said. “But at the moment, there aren’t really any concrete actions to develop that recycling industry.”

The country doesn’t have any cathode or anode production, according to Benchmark’s Cathode and Anode forecasts. Though, without a larger cell production base, there is little to incentivise cathode and anode producers to the UK.

What’s clear is that although the UK has elements of strategy, for the country to succeed in becoming a relevant player in the European and global battery scene these need to be aligned and backed with investment.

Subscribe to Benchmark Source

This is a Benchmark Source article. Fill in the form below to request a free trial:

For more information about the service this data draws from, get in touch

Want to read more analytical content?

Create a Free Account

Create a free Intelligence account to access 3 content pieces per month.